The new American century

Flashing global economic warning lights offer historic opportunity for USA

US GDP per capita growing faster than any other country

nearly 60% of global foreign exchange reserves still held in dollars

number of jobs “reshored” in 2023 will reach 40% of what US lost since 2010

🚀 Please smash the ♡ button, subscribe for the banter ✓ and share with friends and colleagues. We are always grateful for your comments and support.

Flashing red lights are warning of a global recession, interest rates are at 22-year highs after inflation hit 9% last year, there is war and energy crisis in Europe, while China manages a significant economic slowdown.

These destablizing shocks present an historic economic opportunity for America.

The fundamentals underpinning America’s economy — from energy to demographics, innovation to the US dollar — mean the country looks set to be the dominant economic player in the next decade, establishing another new American century.

And, most importantly for investors, the US appears to be seizing the opportunity.

Secure and low cost energy

The critical nature of energy for any economic growth has been thrown into sharp relief by the Russian invasion of Ukraine and the effective weaponization of gas and oil supplies, especially against Europe.

Natural gas prices in Europe spiked to record levels after Russia shut off most of its gas exports to the country (our analysis on how the global natural gas network is being overhauled).

Germany, the economic engine of Europe, is now threatened with de-industrialization. One study, by the Berlin-based think tank Dezernat Zukunft, warns the country could lose up to €120 billion in economic output and 1.3 million jobs, if energy prices remain high.

The US, in contrast, has been a net total energy exporter since 2019, for the first time since 1957. Much of this growth has come from the shale revolution, using hydraulic fracturing and horizontal drilling to access new fields of oil and gas.

And, demand for American energy is on the rise, with the US now the world’s largest LNG exporter (our analysis on how the US is supplying LNG demand from Europe and Asia).

The US is also rapidly building out it’s renewable energy sector, with the share of US renewable electricity generation set to increase from 21% in 2022 to 24% in 2024, as well as pledging to triple it’s nuclear energy capacity by 2040.

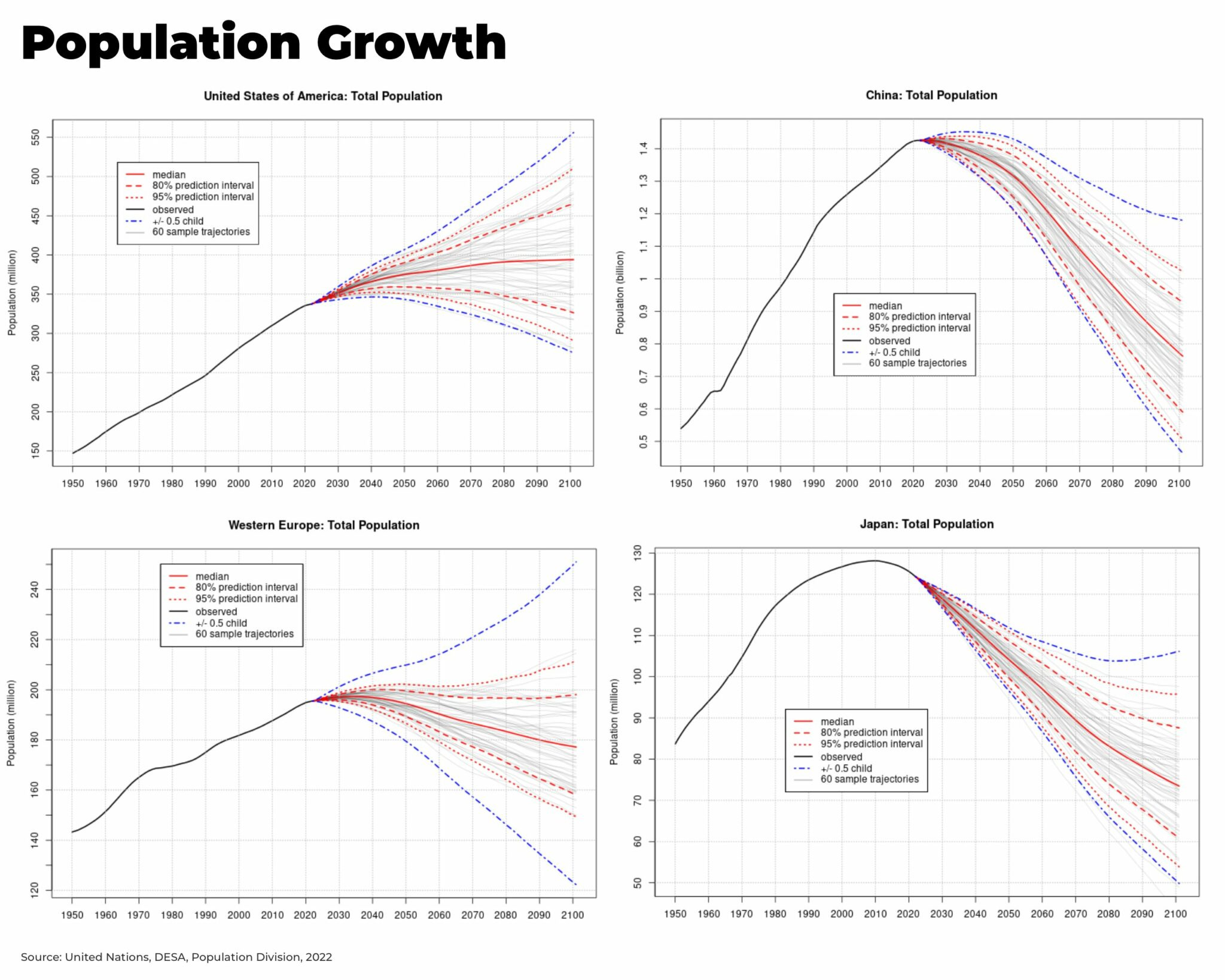

Demographics

The US is one of the few major economic regions to have relatively stable population growth. Newly revised population figures by the UN’s Department for Economic and Social Affairs suggest America may well see a decline in its population, but nothing in comparison to its major economic rivals, Europe, China and Japan.

China’s head of population for the National health Commission confirmed the country should expect negative growth, with the population starting to decrease before 2025.

Population figures do not mean America’s economy is destined for growth — plenty of smaller countries have great wealth, and countries with much larger populations like India have struggled for growth — but, together with immigration, the US has a younger, more productive population to stay competitive.

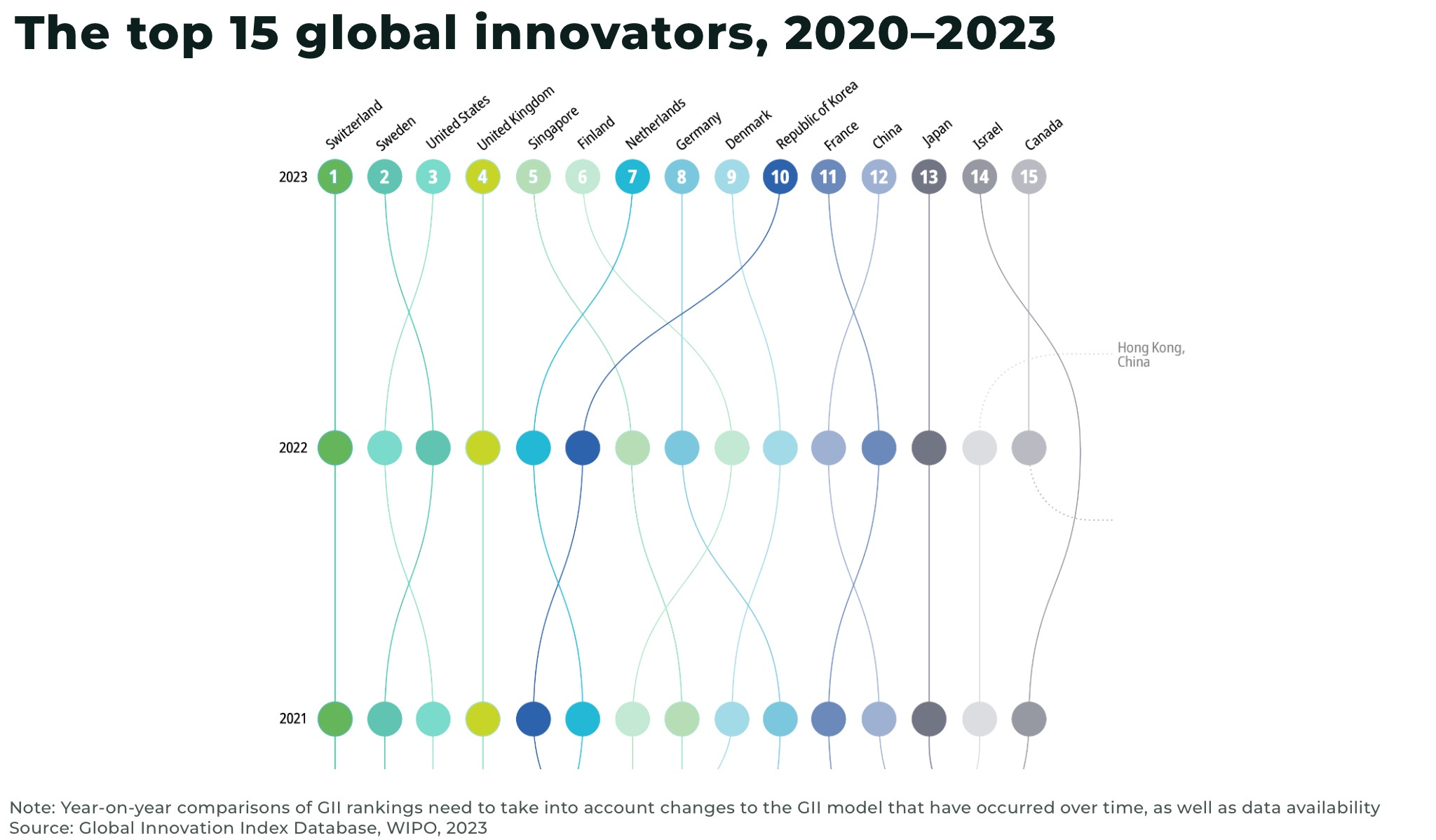

Innovation

The US is competing for second place in the 2023 World Intellectual Property Organization’s (WIPO) Global Innovation Index. China, for example, is in twelfth place.

And, out of the top most innovative companies in the world in 2023, the top 6 are all American. Only two are from China.

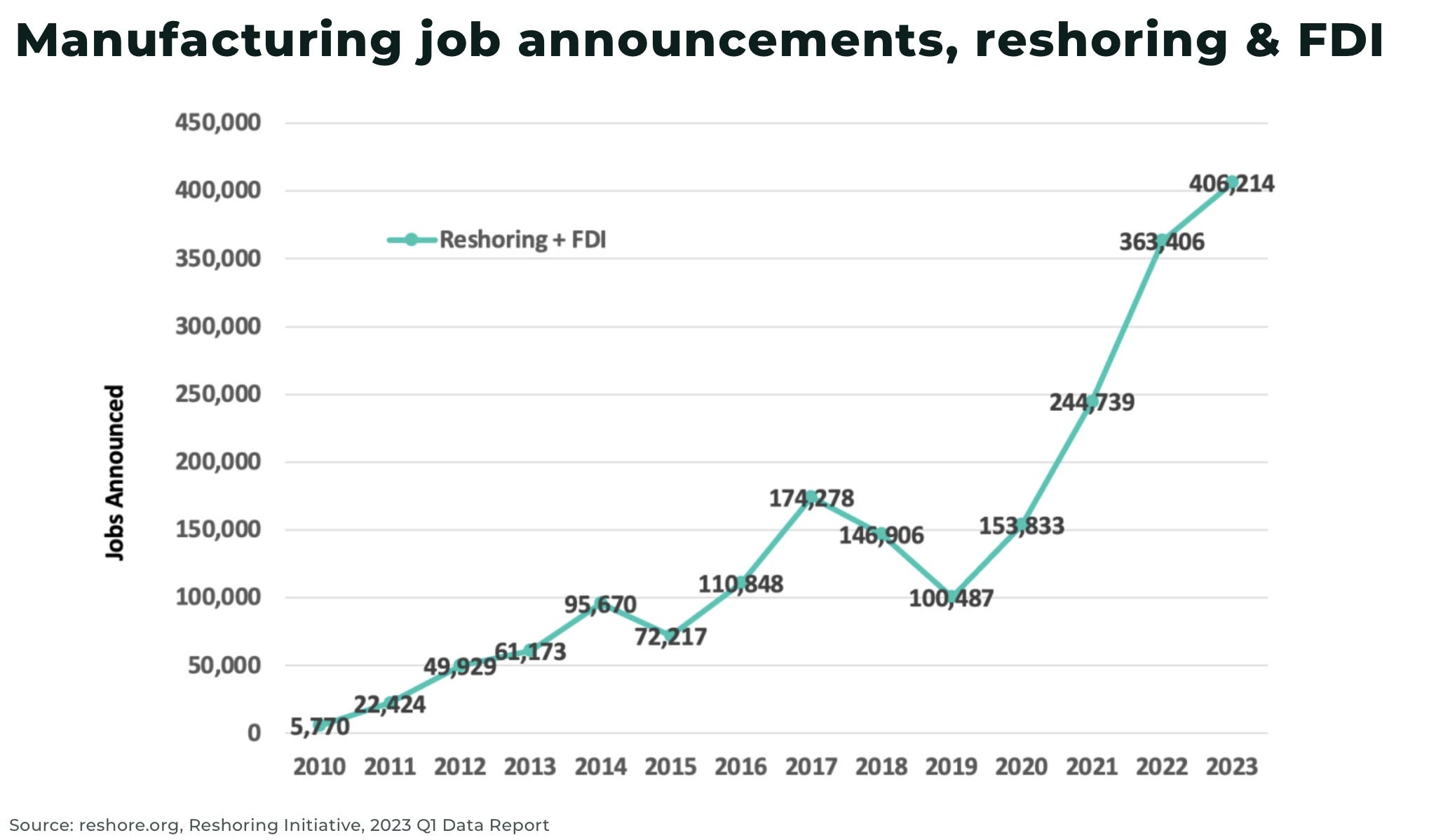

Supply chains and manufacturing

The Covid pandemic, Russia’s invasion of Ukraine, as well as demands to meet climate change goals, have highlighted serious threats to global supply chains, including rising costs of raw materials and freight, to export bans, tariffs, labour shortages and rising wages.

The US is now working to seize the initiative to secure it’s supply chains adn manufacturing base.

According to one recent report, the number of jobs brought back since the manufacturing low in 2010, will reach about 40% of what the US lost to offshoring by 2023.

It’s a move supported by both Republicans and Democrats in the US. For example,

President Biden boasts the economy has added around 800,000 manufacturing jobs since he took office

the bipartisan US$1.2 trillion Infrastructure Investment and Jobs Act, promises to rebuild transport networks and the power grid

We, of course, do not expect all manufacturing to return to the US, but the direction of travel towards more secure, domestic supply chains is clear with no signs of slowing down, even if some of those domestic jurisdictions are in allied countries such as Canada and Australia.

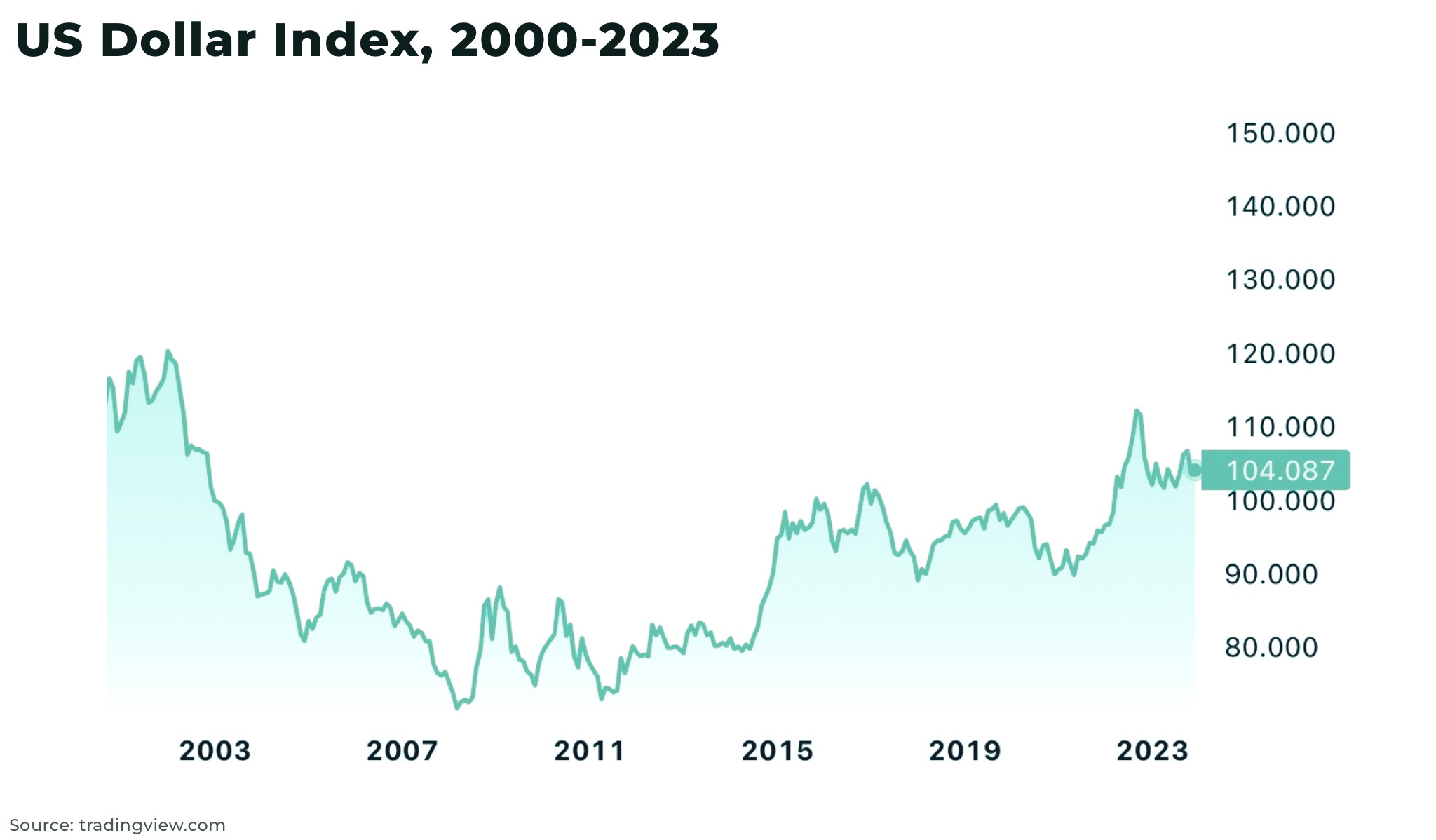

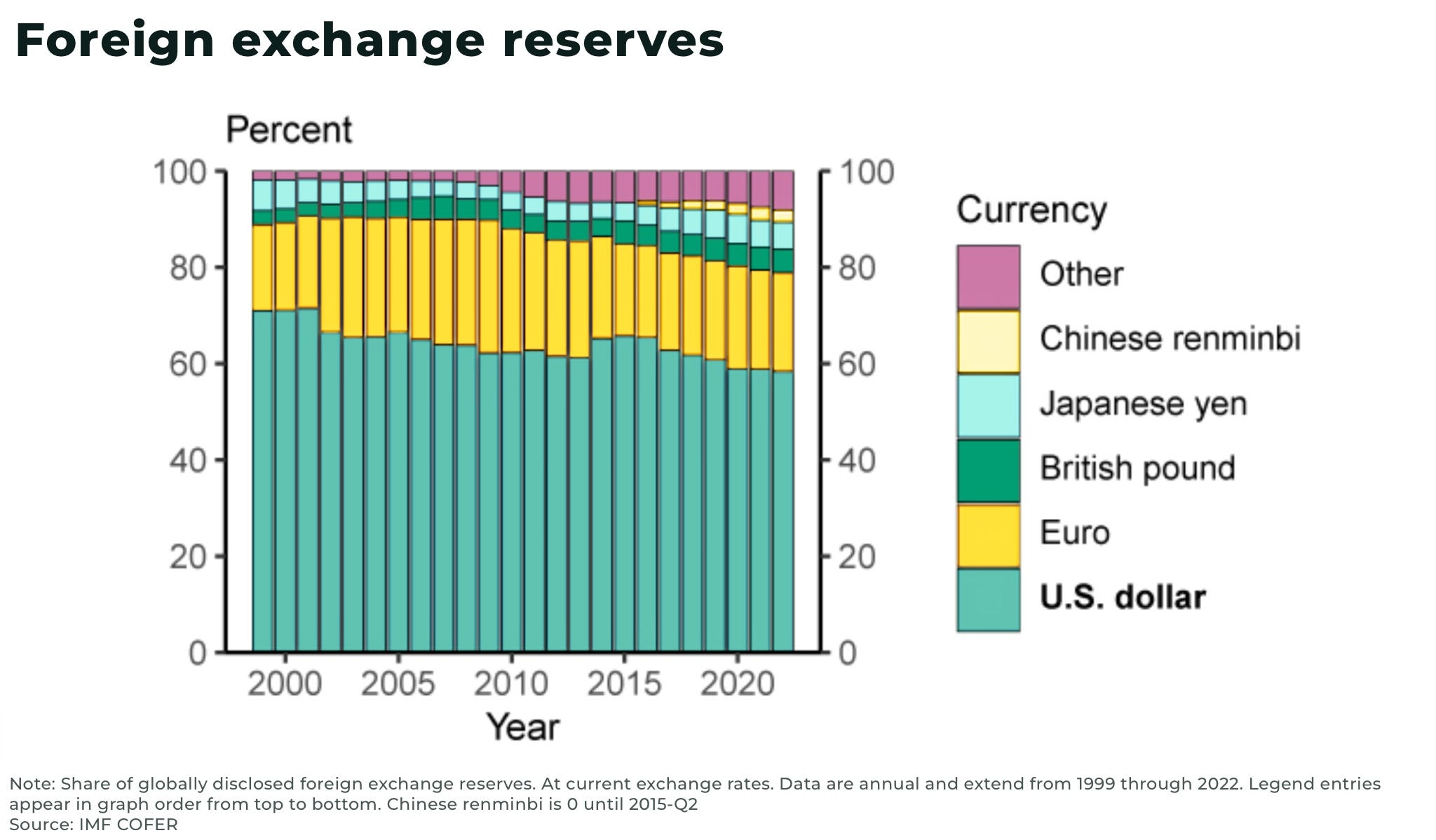

The US dollar

There have been many warnings of the demise of US dollar as the global reserve currency, but the DXY, an index of of the US dollar against other major world currencies, is at a 20-year high.

And, nearly 60% of global foreign exchange reserves are still held in dollars.

As we suggest in our recent newsletter, the dollar is not about to lose it’s place as the global reserve currency anytime soon.

After Russia invaded Ukraine, the Inflation Reduction Act of 2022 introduced renewable and electric vehicle tax credits, and the Fed raised interest rates to tackle record inflation, capital has poured into the US, pushing up the dollar.

The effects of a strong dollar will have a significant impact across the world, but it’s the sentiment that’s critical: confidence that, in times of trouble, the world still views the dollar as the most secure currency, not just because of a greater degree of transparency and trust than other rival currencies, because of America’s economic and military might.

For example, the Euro is the second most widely held currency in reserves after the dollar and they are also raising interest rates. But, after the eurozone crisis in 2009 and now the regional energy crisis, many investors are wary — with the Euro reaching parity with the dollar for the first time in 20 years.

The Chinese Renminbi currently remains too limited by liquidity and capital controls to act as a global currency.

And this is important because it means the US can continue to borrow money at a lower cost, extending the influence of US financial institutions, as well as increasing American financial leverage through access to the US financial system or sanctions, such as it has recently done with Russia.

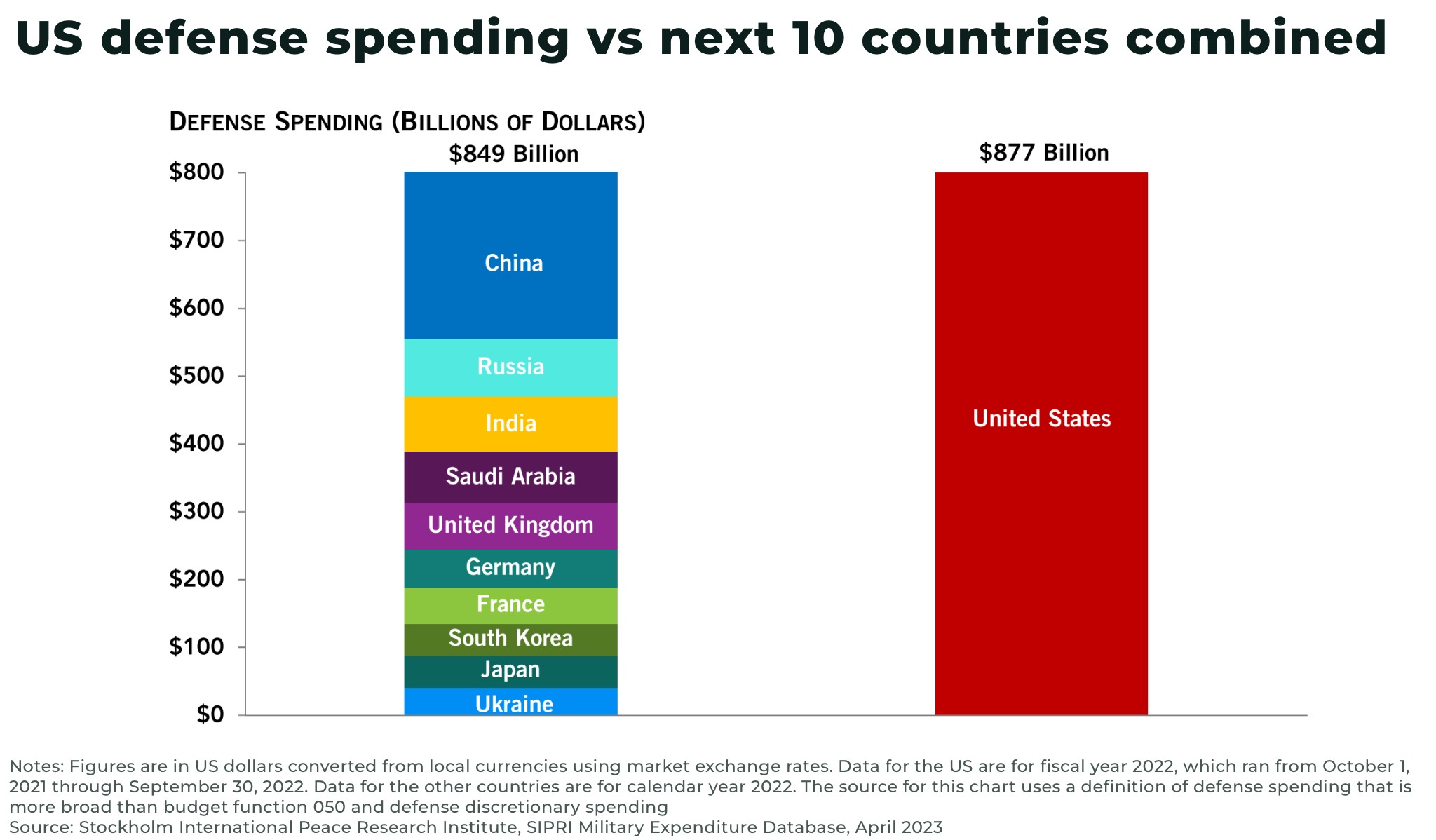

The US military

The US spends US$877 billion on it’s military, more than the next 10 countries combined.

This allows the US to boast it can afford to support Ukraine and Israel in their wars against Russia and Hamas respectively, soon after ending two other wars in Iraq and Afghanistan, while also maintaining commitments to more than 750 bases in at least 80 countries, as well as a military deterrence against China.

No other country on earth — or in history — can compare with the military projection capacity of the US.

A recent report on “Does the US Economy Benefit from US Alliances and Forward Military Presence?” concludes the US would have experienced a roughly 0.4% decline in consumer purchasing power in 2006 had it exited NATO five years prior rather than sustaining its NATO commitments.

But this underplays the massive role US military has played in securing global supply chains and regional peace since the end of the Second World War, the end of the British Empire, and then then end of the Cold War.

Rule of law

Enterprise thrives in a stable, secure environment where businesses have legal means to protect their interest. It’s not perfect, but the US still upholds this value. And we do not see this changing in the foreseeable future, whatever the political outcomes in the short and medium term.

It’s the same in Europe, but business in many other countries operate under “rule by law”, with the government often having final say over property and capital.

Conclusion

We expect the next decade to be extremely volatile with the end of zero-interest rates, inflation, rising geopolitical tensions, and a slowing global economy — and there may well be more black swan events on the horizon.

Other challenges include:

global growth forecast to slow from 6.1% in 2021 to 3% in both 2023 and 2024

political volatility, not just in the US

US debt interest payments above US$1 trillion yearly pace as borrowing continues to rise

The US faces a number of significant challenges in the years to come. However, these are challenges that nearly every other country is also grappling with, as they too contend with a multitude of issues, ranging from demographics to innovation – areas where the US looks set to maintain its global leadership.

So, for investors unsure where to put their money to secure growth, the long-term fundamentals underpinning the US are flashing “buy”.

🚀 Please smash the ♡ button, subscribe for the banter ✓ and share with friends and colleagues. We are always grateful for your comments and support.

Great article! I share your optimism for America, as do a couple of geopolitical strategists and authors I follow closely, Peter Zeihan (The End of the World is Just the Beginning) and George Friedman (The Storm Before the Calm). I also share your expectation for a highly volatile decade, as does demographer Neil Howe (The Fourth Turning is Here: What the Seasons of History Tell Us about How and When This Crisis Will End) and social, complexity, and cliodynamics scientist Peter Turchin (End Times: Elites, Counter-Elites, and The Path of Political Disintegration). I look forward to following The Oregon Group and referencing your work in my Substack.