Where will new uranium supply come from?

Uranium demand expected to increase 200% by 2040

uranium demand set to increase 200% by 2040

uranium prices already at 15-year highs on tight supply

ore grade and mining bans across globe limiting new supply

Canada's Athabasca Basin contains world’s largest, high-grade uranium deposits

🚀 Please smash the ♡ button, subscribe for the banter ✓ and share with friends and colleagues. We are always grateful for your comments and support.

Demand for uranium is expected to expand 28% by 2030 and nearly 200% by 2040. Tight supply and rising demand has already significantly impacted prices with 15-year highs of more than $80/lb.

According to our latest industry report, The Start of the Uranium Bull Market and the Second Atomic Age, uranium prices are at the start of a 10-year bull market.

So, where will new uranium supply come from to meet this new demand?

Uranium supply vs demand

Firstly, why is supply of uranium so tight and demand rising?

Supply issues include:

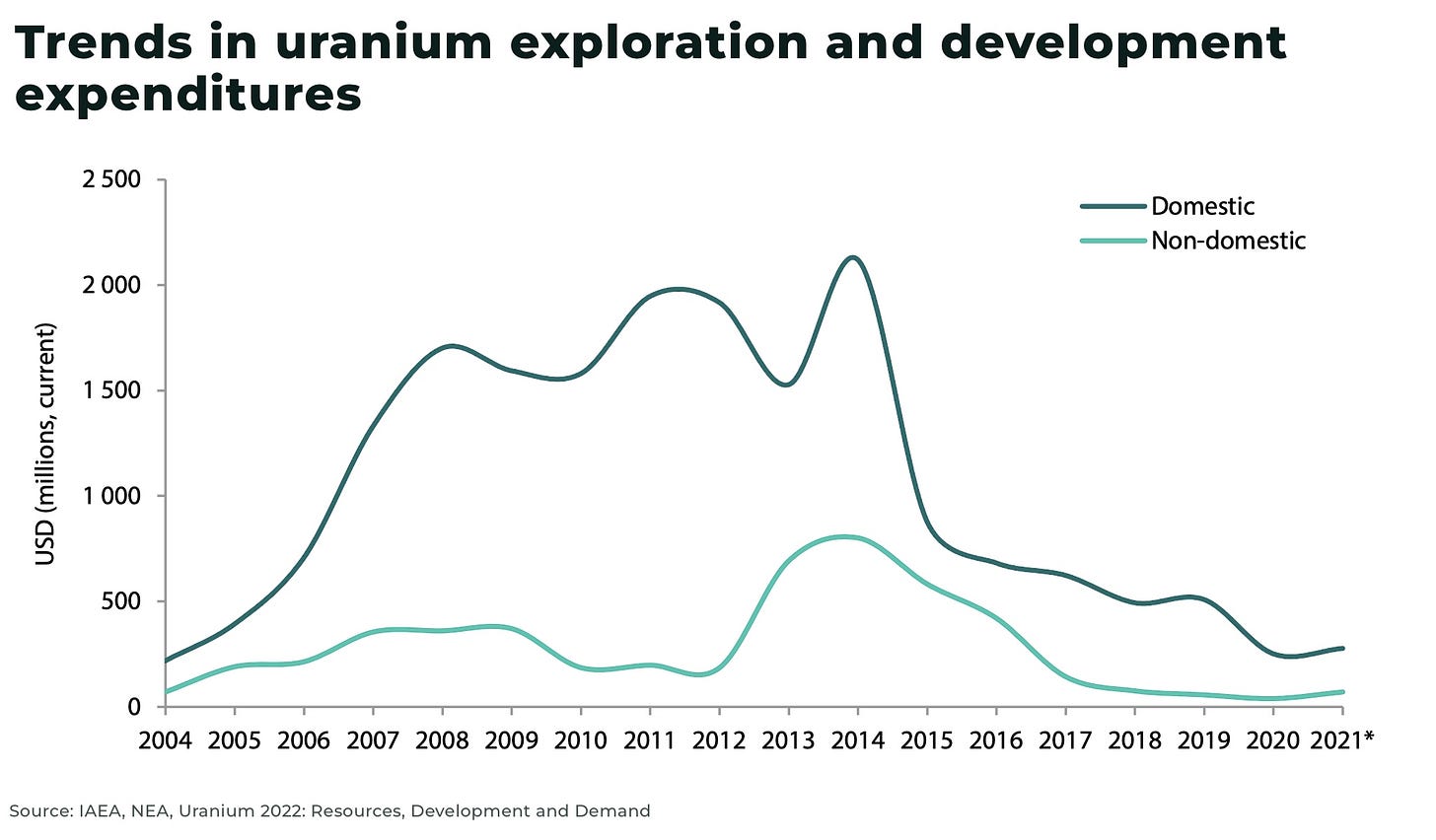

investment in uranium exploration and mine development has fallen steadily over the last 10 years, especially after the Fukushima accident in 2011, as well as focus by governments on renewable energy sources to reach net-zero targets

Western sanctions on Russia have complicated the import of Russian uranium, with threats of banning imports into the US completely

in the last year, inflation and interest rate rises also increased costs for new and existing uranium mine projects

conflict in Niger cut off 5% of the world’s uranium, representing more than 24% of the EU’s uranium imports

But, announcements for new nuclear power projects have been coming at a historic high. To highlight just some of the biggest examples:

more than 20 countries, across 4 continents, have pledged to triple global nuclear capacity by 2050

China plans at least 150 new reactors in the next 15 years, at a cost of more than US$440 billion more than the rest of the world has built in the past 35 years

India announced this year, plans to increase nuclear capacity from 6780 MWe to 22,480 MWe by 2031, with nuclear accounting for nearly 9% of India's electricity by 2047

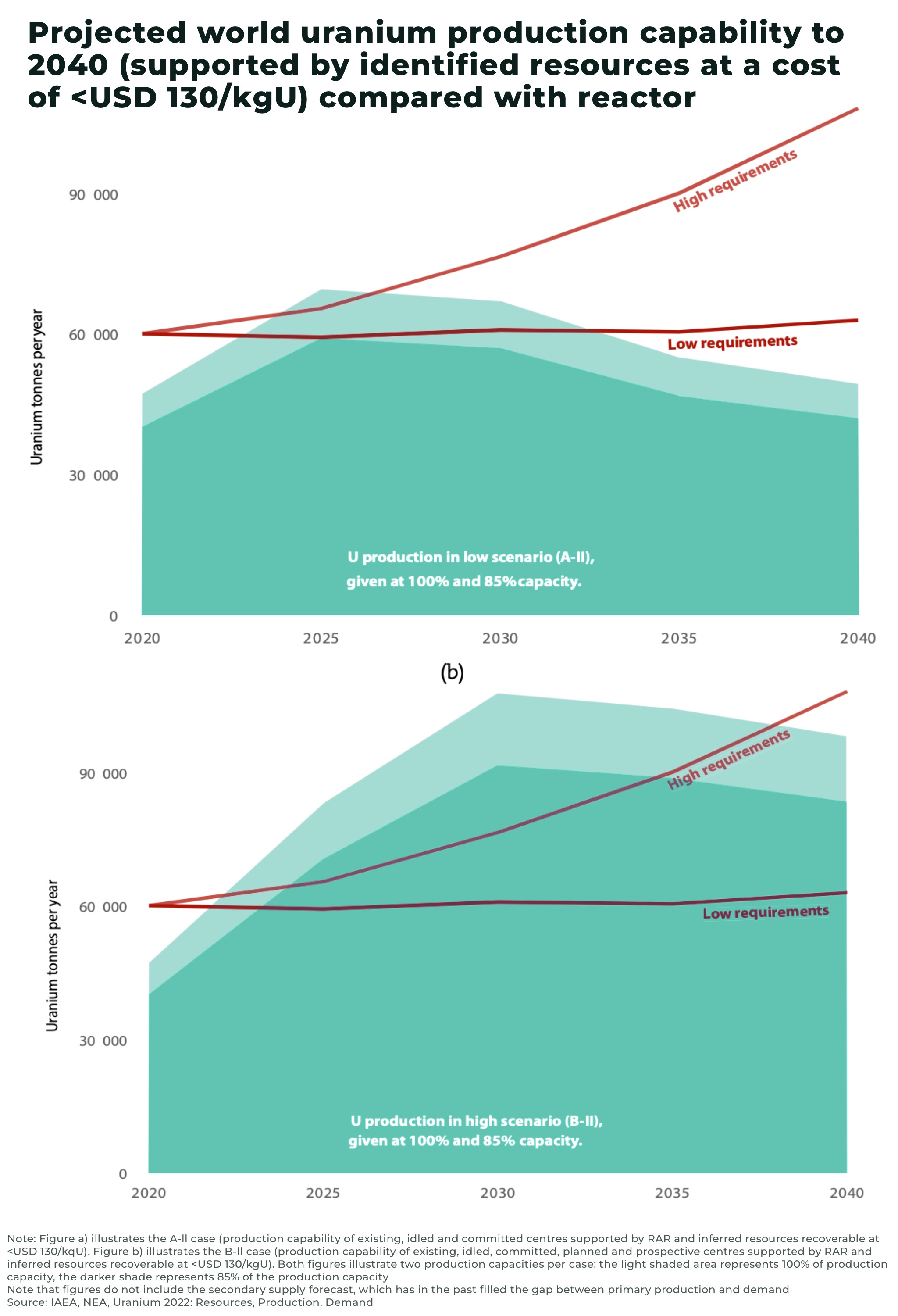

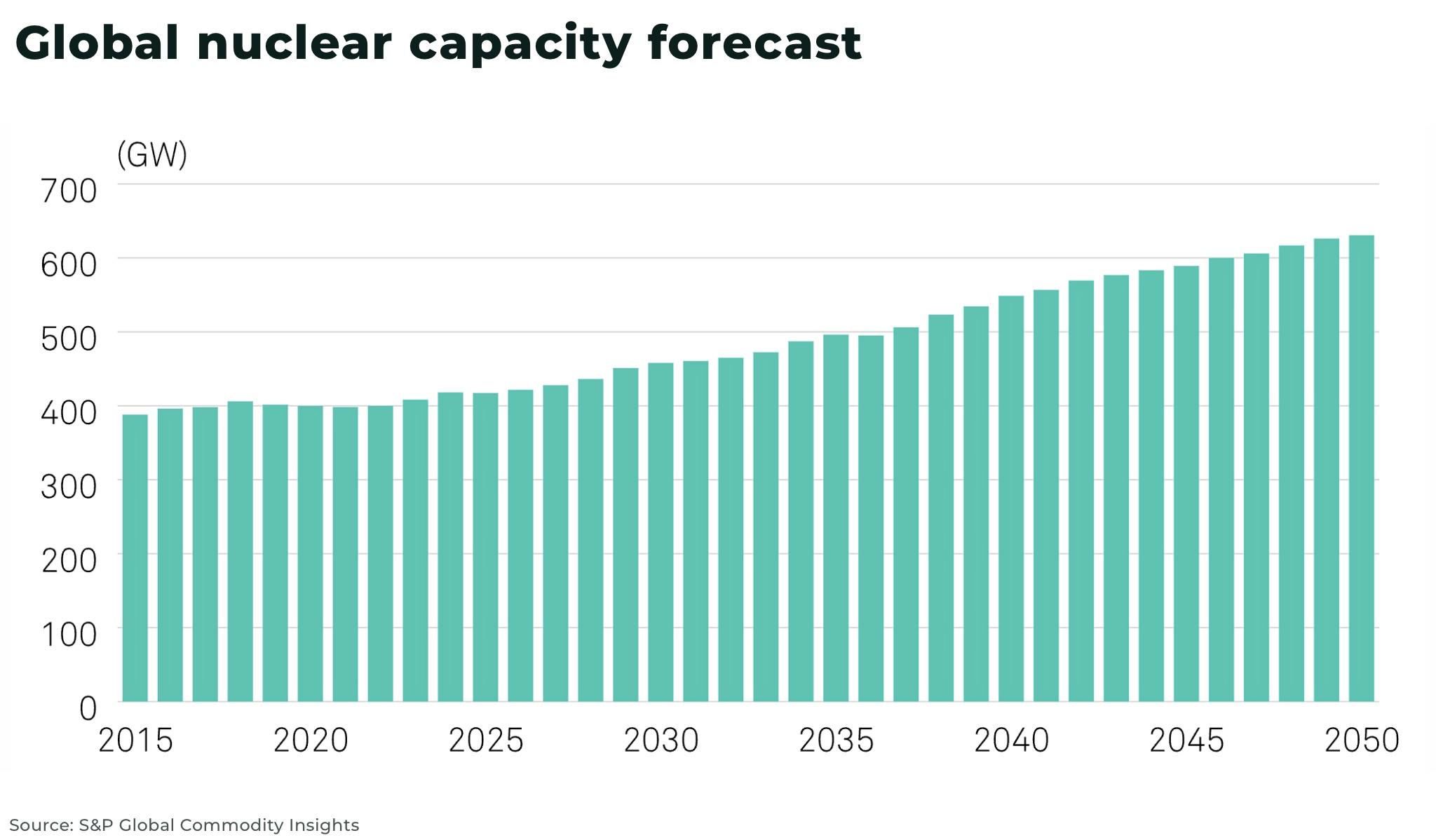

according to the International Atomic Energy Agency (IAEA), nuclear energy capacity is set to expand anywhere from 24% to 100% by 2050, depending on use case scenario. And once these reactors are switched on, they will be using uranium all day, every day for 60–80 years

New uranium supply

So, where can new uranium supply come online fast enough to meet demand? There are concerns over future supply from many of the major producers:

Kazakhstan

Kazakhstan is the largest producer of uranium in the world, with 41% of supply and 12% of global reserves

uranium production from Kazakhstan fell in 2022 by 3% (592tU) year-on-year, and guidance has been cut by 500tU for 2023 due to “wellhead development, procurement and supply chain issues, including inflationary pressure on production materials”

Kazakhstan and China have signed a long-term deal to supply uranium to China, which comes after the National Atomic Company, Kazatomprom, supplied the first batch of uranium assemblies to China earlier this year

We expect continued closer ties between Kazakhstan and China, especially as China looks for a secure of uranium to power it's massive nuclear power build out

Australia

Despite having the largest known uranium reserves in the world, and the fourth largest producer, Australia has a difficult relationship with uranium mining, with it banned in much of the country:

Western Australia state government has a ‘no uranium’ condition on future mining leases. Of the four uranium projects that received State Ministerial approval under the former Liberal National Government, only one has received approval to proceed to next stage of development

New South Wales has had a 30-year ban on uranium mining

Queensland revoked a ban on uranium mining in 2012, only to reinstate it again three years later

There is momentum to overturn some of the uranium mining moratoriums in Australia, but even if they get the go-ahead, it could take between 10-15 years to develop any new mines.

Africa

The world’s third largest uranium exporter in the world in 2022 was Namibia, with production expected to increase by a compound annual growth rate of 5% between 2022-2026.

However, earlier this year, the government announced it is considering taking a minority stake in mining and petroleum producers. It is not yet clear what percentage the country will seek in resource projects.

And, in Niger, the seventh largest uranium exporter in the world, as we highlighted above, a recent coup destabilized exports due to sanctions.

There are, of course, many other mining opportunities, but often the reserves and ore grade are low, geopolitics and supply chains at risk (eg Russia), or significant pressure from local communities and permitting issues to prevent new development or reopening of mothballed mines (eg US), or new sources such as Sweden which has just announced plans to lift a national ban on uranium mining but, as we've flagged, it will take years to build out the mines.

That leaves Canada.

The Athabasca Basin

Canada was the world’s largest producer of uranium until 2009, at which point it was overtaken when Kazakhstan became the world’s largest uranium supplier with the development of massive, low-grade deposits amenable to In Situ Leaching (ISL) extraction. In 2020 Australia moved into second place.

Then, in 2022, Canada became the world’s second largest producer of uranium with 7351 tons, up from third place in 2021 with 4693 tons — an almost 57% increase.

The reason for the dramatic rise: the Athabasca Basin.

Canada’s Athabasca Basin contains the world’s largest high-grade uranium deposits, with grades up to x100 greater than the average ore grade deposits elsewhere in the world.

Canada has known reserves of 588,500 tons across the country, with significant exploration supported by the governments new critical mineral strategy.

There are former mines in Ontario and Quebec, but the majority of the investment in exploration and development is focused on the Athabasca region, an area of almost 100,000 square kilometers, located primarily in the province of Saskatchewan – one of the top rated mining jurisdictions in the world for investment, as well as a small portion of Alberta.

Canada’s Athabasca Basin contains the world’s largest, high-grade uranium deposits, with ore grade between x10-100 greater than the average ore grade deposits elsewhere in the world.

"Saskatchewan's uranium is key as the world looks to transition to sustainable power generation and source minerals from secure, democratic regions"

— Jim Reiter, Energy and Resources Minister

Uranium in Saskatchewan was discovered in 1934 at Beaverlodge in the northwest corner of the province and the province has produced uranium consistently for the last 70+ years.

It already has the world’s largest producing uranium mine, Cigar Lake. Cameco owns 50% of Cigar Lake which boasts an average U3O8 grade of 15.9%. With 2021 production forecast to be 12 M lbs (6 M net to Cameco), it would make this single mine account for roughly 11% of global uranium production. As well as a a mill (Orano’s McClean Lake mill), the world’s largest and Canada’s only uranium refinery is located at Blind River, Ontario, where uranium ore concentrates from Canada and abroad are refined to produce uranium trioxide.

The region is also host to junior companies — at least 34 at last count — highlighting the potential promise of the region for investors.

Importantly, the Athabasca Basin sits at the strategic centre of Western critical mineral supply chains:

approximately 85% of Canada’s uranium production is exported, predominantly to the US, Europe, and then Asia

as part of a Free Trade Agreement with the US, Canada has access to new tax credits to develop mines

and, domestically, Canada is set to significantly expand it’s own nuclear power fleet, for example the expansion of Bruce Power in Ontario to be the world's biggest reactor

How should investors position themselves to gain exposure

Globally, there are, of course, the ETFs as well as buy-and-hold players like the Sprott Physical Uranium Trust and Yellowcake, as well as current producers like Kazatomprom, offering exposure to the uranium opportunity, including existing cash flow.

For investors looking specifically at Canada, the Athabasca Basin offers two main opportunities:

eastern Athabasca offers greater security and less risk with established mines and companies, such as Cigar Lake Mine, Key Lake mine and McClean Lake mine

western Athabasca offers major new uranium discoveries at an advanced stage of development, including NextGen Energy, Fission Uranium, and Purepoint Uranium

We caught up with Fission Uranium CEO, Ross McElroy, to discuss the move for investment from east to west Athabasca Basin:

Investors have, until recently, shied away from the western basin due to concerns over a lack of infrastructure. Specifically, while there is a provincial government maintained highway that runs right next to Fission’s project and close to NextGen’s, there’s no mill.

But, this was not always the case, as there was once a producing mine and mill at Cluff Lake, some 70 km north of NextGen and Fission — which is why there is, in fact, a highway there.

And now, NextGen and Fission are racing to build new mills, so it looks increasingly likely that one, or even two mills, might be built and operating by the end of the decade.

We’ve seen some chatter that the Government might only issue one mill permit, or make permitting for both projects conditional upon the companies combining into one, all because the projects are so close. We can’t speak for the Government, but will point out that, while mergers or at least cooperative agreements tend to be the norm under these circumstances, we can think of a variety of adjacent projects that have gone into production — both with their own mills — and there’s no Provincial or Federal limitations in Canada that would prevent such a situation.

Before the end of the decade, projects owned by Denison Mines which is on the eastern side of the Basin, as well as NexGen Energy, and Fission Uranium have the potential to enter production. Denison is trialing a form of ISL for extraction and has to contend with ore that possesses a very high level of arsenic. This leaves the projects of NexGen and Fission Uranium.

As ever, especially with junior mining companies, make sure you do your own due diligence.

The projects are side by side and together could bring approximately 40 million lbs of uranium per year onto the market — that’s a lot of new supply — but, by the time they come online, the need for new sources of uranium will be urgent.

🚀 Please smash the ♡ button, subscribe for the banter ✓ and share with friends and colleagues. We are always grateful for your comments and support.