US miners vs US automakers

Caught between the drill bit and the assembly line in the coming EV trade war

🚀 Please smash the ♡ button, subscribe for the banter ✓ and share with friends and colleagues. We are always grateful for your comments and support.

US miners and US automakers are on a collision course over supply of critical minerals for electric batteries.

The reason: a “flood” of electric vehicles from China.

Chinese electric vehicle exports threaten to divide US automakers and miners over the seemingly inconspicuous section 30D of the US Inflation Reduction Act — or, what critical minerals can be sourced from so-called “Foreign Entities Of Concern”.

What is Section 30D

To be eligible for a US$3,750 tax credit on electric vehicle (EV) sales in the US, provided by the Inflation Reduction Act (IRA) in 2022, a percentage of critical minerals an electric battery must be extracted or processed in the US or a country with a free-trade agreement (FTA) with the US. The required percentage is set to rise every year until 2027:

for 2023, applicable percentage is 40%

for 2024, applicable percentage is 50%

for 2025, applicable percentage is 60%

for 2026, applicable percentage is 70%

from 2027, the applicable percentage is 80%

The percentage increases every year to allow time for miners and automakers to build out supply and demand capacity. For example, this year, there simply is not enough supply of the relevant critical minerals from US sources to economically build enough EVs.

However, the inherent tension in this regulation is already threatening to undermine the strategy. In particular, the application of Foreign Entity of Concern (FEOC) — China, Russia, Iran, North Korea — credit eligibility exclusions.

From 2024, any vehicle that contains critical minerals from an FEOC will be ineligible for the tax credits worth up to US$3,750 (and another US3,750 if the battery components are manufactured or assembled by an FEOC, totaling US$7,500 worth of tax credits).

The problem

The US and its free trade partners (eg Australia and Canada) cannot produce enough critical minerals at competitive prices and in high enough quantity, compared to China’s critical mineral supply chains.

For example, nickel mines are closing across Australia and the West in the face of oversupply from Indonesia and China — see our analysis on “The Great Nickel Trade War”.

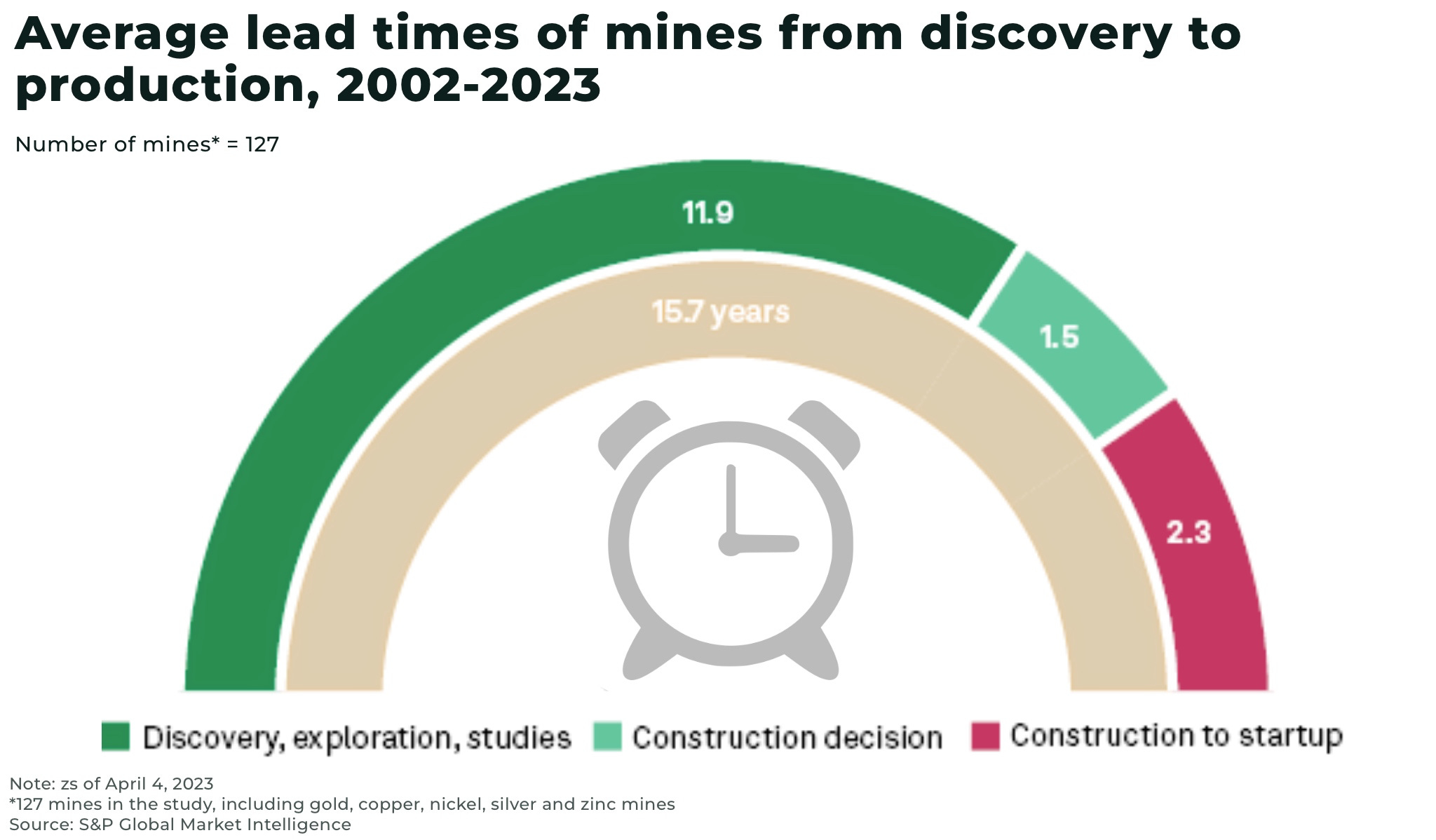

To develop a new mine in the West takes, on average, over 15 years. The Biden administration has moved to fast-track the approval and permitting process for critical mineral mines but, even if the process is speeded up, it will still take years.

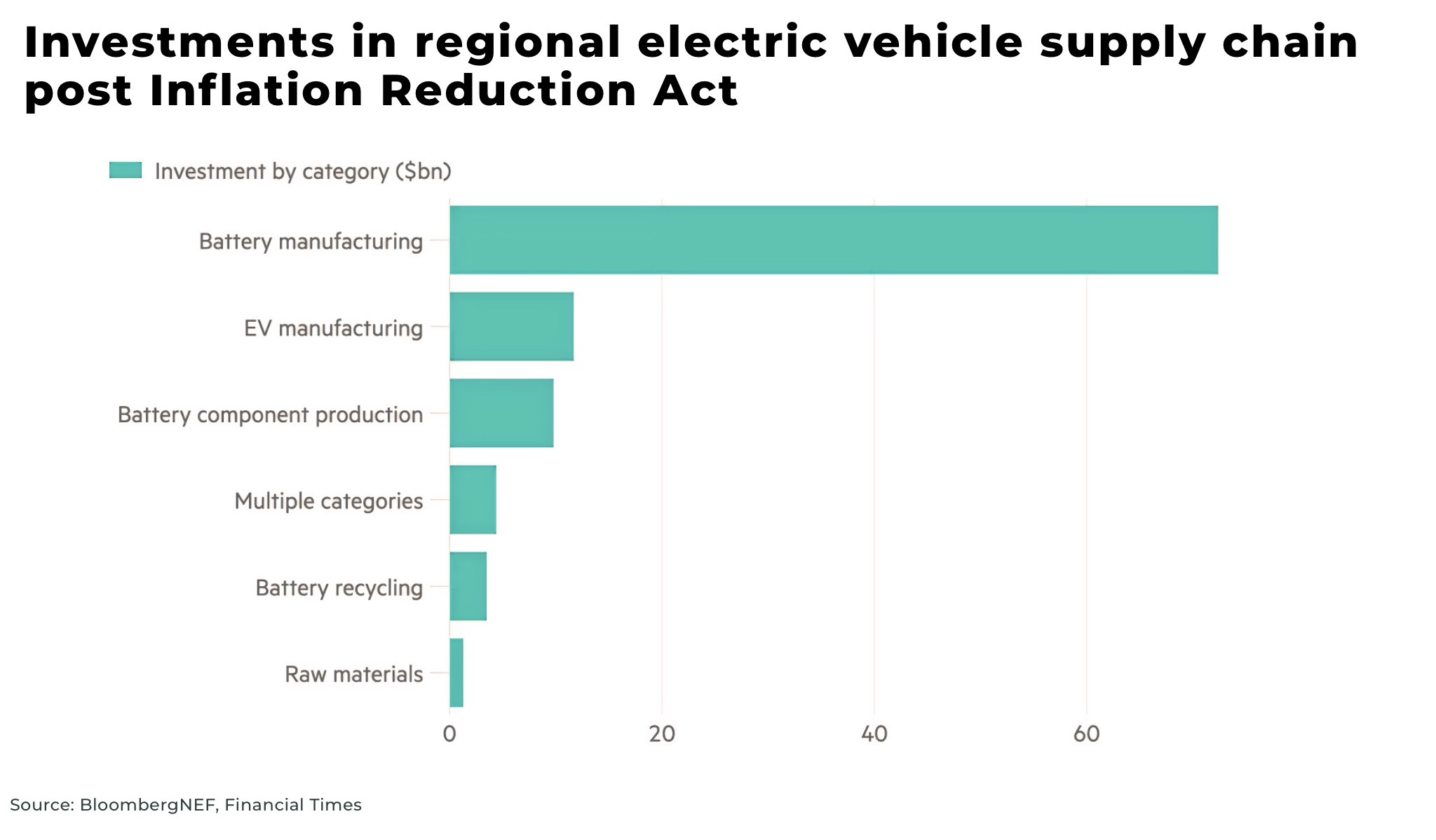

In the meantime, an estimated US$100 billion has been announced in electric vehicle and battery manufacturing in the US in the last 8 years, 54% since the IRA was passed in 2022, with demand for EVs forecast to rise sharply over the next decade, expected to reach 16.7 million in 2024.

In comparison with a new mine, it only takes approximately 2 years to build a new giga factory.

But the need for a plentiful, cheap supply of critical minerals by US automakers became an urgent priority this year as EV sales and exports from China surged.

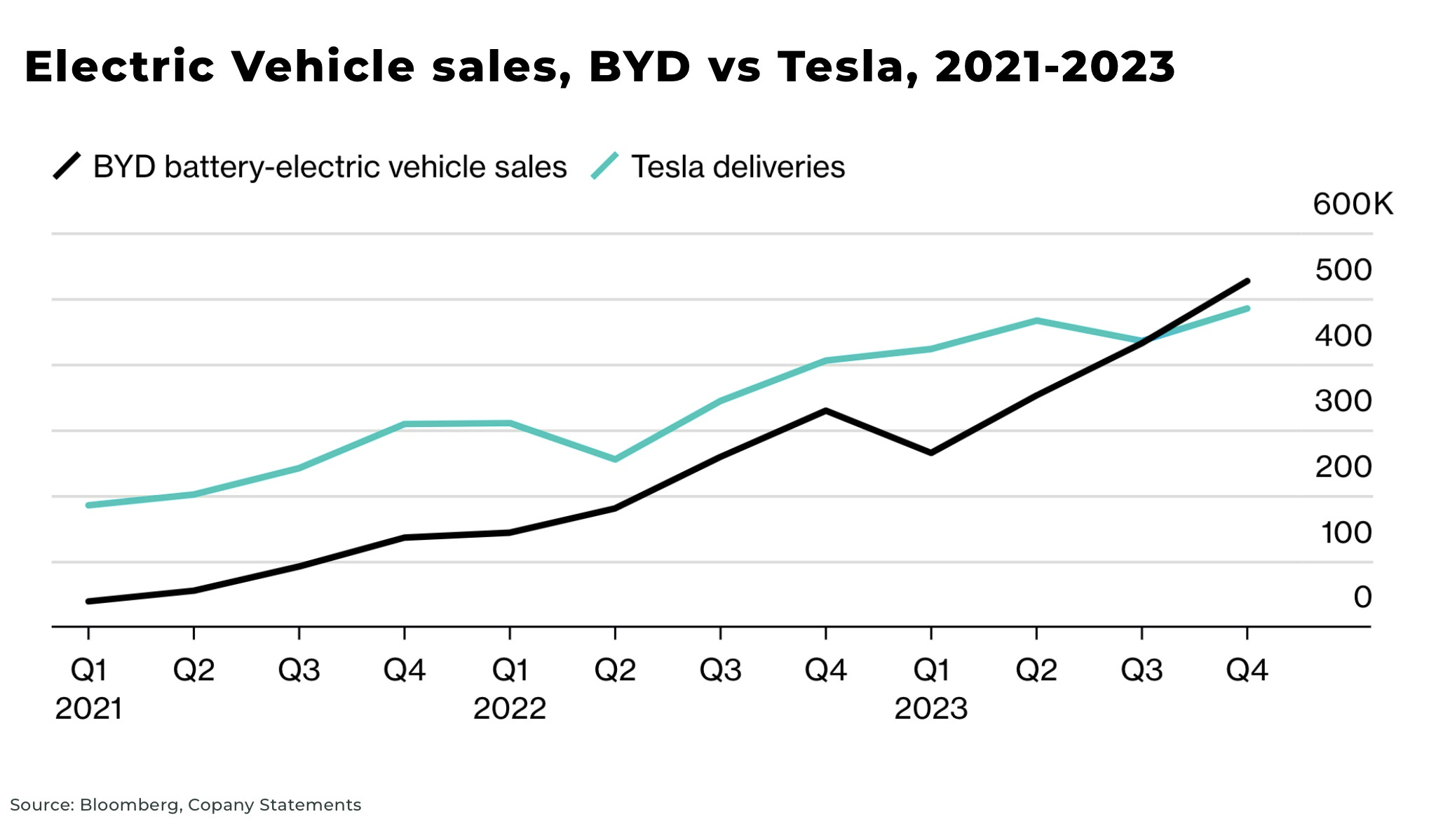

Chinese automaker BYD sold more electric vehicles than Tesla in the last 3 months of 2024. UBS estimates China's global market share will double to 33% by 2030, and the share by Western automakers will fall to 58% (from 81% in 2023).

“The Chinese offensive is possibly the biggest risk that companies like Tesla and ourselves are facing right now. We have to work very, very hard to make sure that we bring our consumers better offerings than the Chinese”

— Carlos Tavares, CEO of Chrysler parent Stellantis NV, told reporters in February

There are a variety of reasons for the success of Chinese EVs, from quality, turnover time for new models, etc, that have put US automakers like GM and Ford on high alert — but the main competitive concern is price.

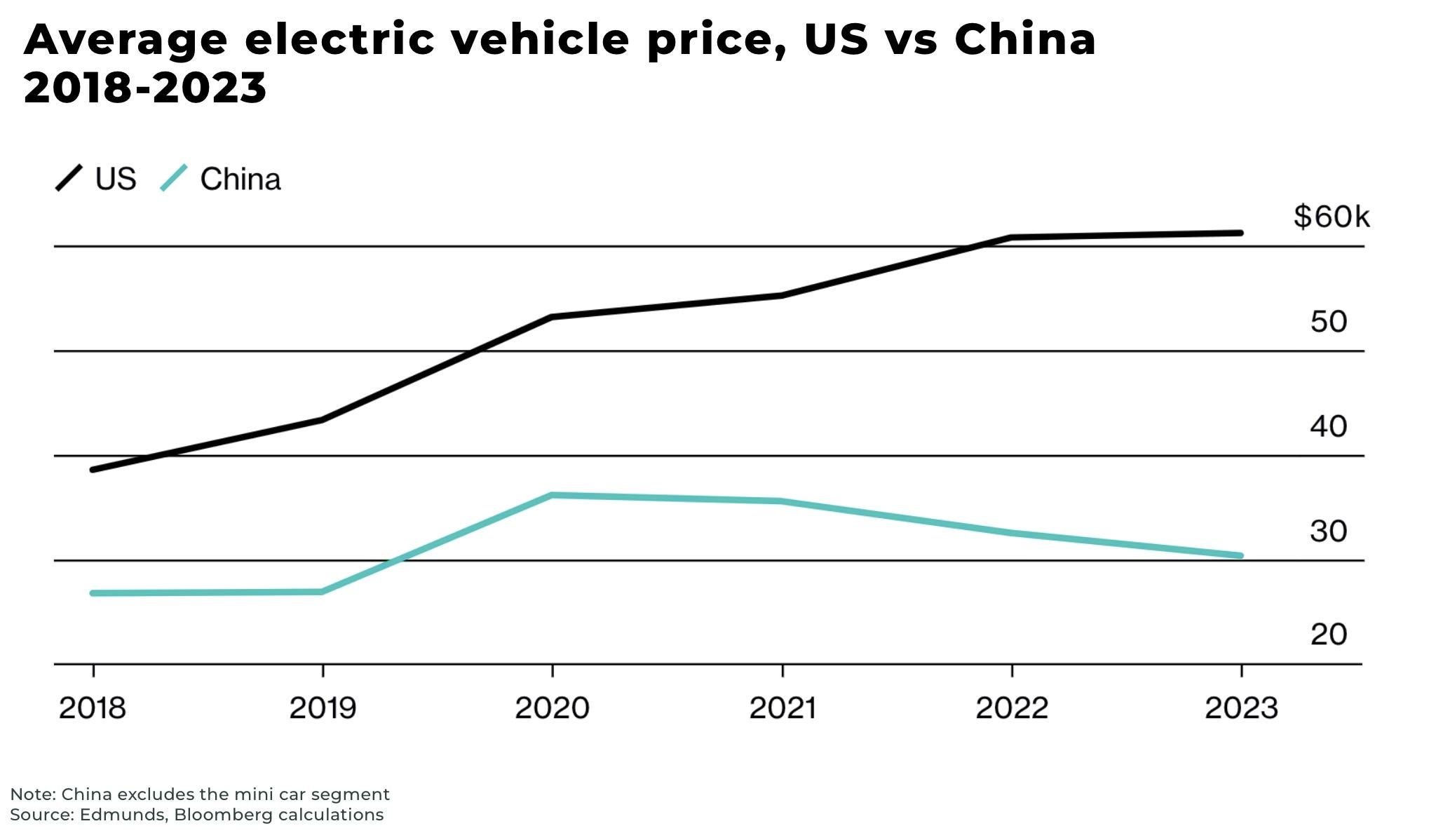

The average cost of an EV in China is about US$35,000, versus more than US$53,000 in the US. UBS estimates BYD has a 25% cost advantage over US and European brands, even despite shipping and trade tarrifs. This month BYD cut prices across 100 models, with the company’s most affordable EV, the Seagull now less than US$10,000, undercutting the average price of an EV in the US by more than US$50,000.

The reasons for this lower price advantage include significant Chinese government subsidies and lower labour costs — as well as accessibility to a cheap, abundant supply of critical minerals.

The US car industry is already sending a warning:

"If there are no trade barriers established, they [Chinese automakers] will pretty much demolish most other car companies in the world… They're extremely good"

— Elon Musk, Tesla CEO, said on a post-earnings call with analysts

“China is unleashing a torrent of heavily subsidized cars upon the world, and America’s auto industry stands squarely in the path of devastation… Existing U.S. tariffs and trade action have staved off an extinction-level event for the US auto industry… but China’s predatory trade practices know no bounds"

— the Alliance for American Manufacturing has warned

And in Europe, Renault CEO is calling for “a European Marshall Plan” warning the continent was facing an “onslaught of electric vehicles from China.”

Tariffs

In 2018, US President Trump imposed a special 25% tax on China-made vehicles, on top of the established 2.5% on all foreign-made cars.

President Biden is reportedly considering increasing these tariffs, as well as launching an investigation into whether Chinese-made cars pose a national security threat.

Donald Trump is threatening a 100% tariff on Chinese-made cars from Mexico if he wins the US presidential 2024 election.

So, regardless of who wins the next US election, we expect a new trade war.

China, for its part, has filed a complaint against US electric-vehicle subsidies with the World Trade Organisation, calling them discriminatory.

Critical minerals

But what about the critical minerals essential for US automakers to compete in both capacity and cost against Chinese cars?

Both the US government and US car industry are making investments into domestic critical mineral supply, for example:

General Motors will invest US$650 million in Lithium America’s to develop the largest lithium mine in the US, as well as lithium deals with Albemarle, Compass Minerals, and others

Panasonic Energy and General Motors are investing a combined US$50 million in Nouveau Monde Graphite which will sell 36,000 metric tons a year of graphite from its facility in Canada

Tesla has signed a deal to buy graphite from a new graphite processing plant built by Syrah Resources

The challenge: is the investment in critical mineral mining across the US and its free-trade markets enough to offset the IRA critical mineral restrictions that will reach 80% in 2027.

To put the challenge in context, in 2022, out of 50 critical minerals, the US was 100% net import reliant for 12, and had an import reliance greater than 50% for 31 others.

There are a significant number of variables that impact the outcome, from how quickly the US EV market grows to the outcome of the US election.

But the truth is that, if current demand forecasts are correct, then no, Western critical mineral capacity will not be enough to meet the forecast demand by 2027, especially in any meaningful way to make the industry economically competitive against China.

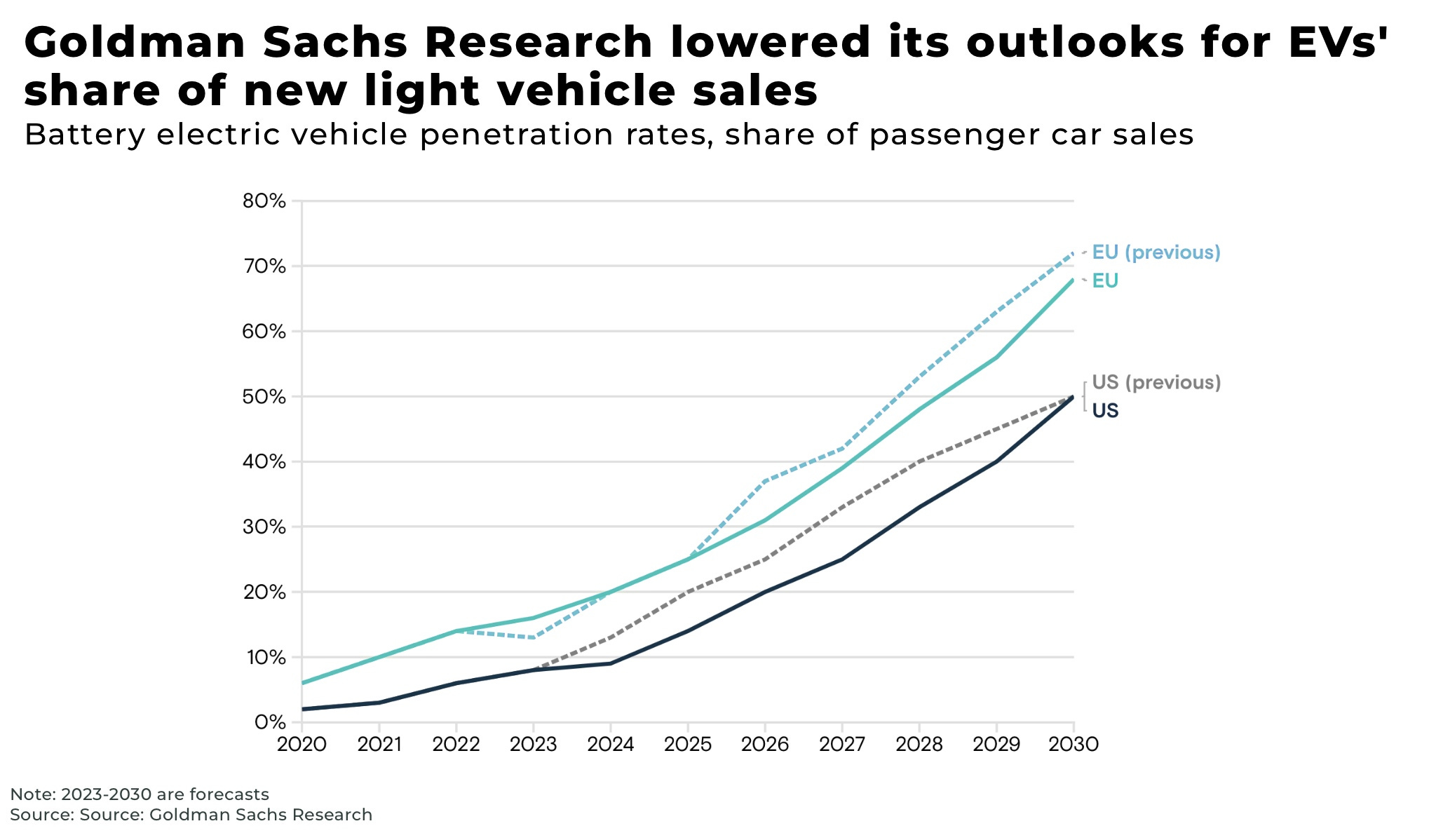

Strict new regulations by the US Environmental Protection Agency on vehicle emissions are projected to mean EVs make up make up 35-56% of sales in vehicles by 2032.

So, for example, Goldman Sachs have lowered their EV sales forecast as growth in the industry slows, yet they are still expected to reach over 50% market penetration by 2030.

Foreign Entity of Concern, Section 30D

And here is the tension between US automakers and US critical mineral miners.

Miners are unlikely to be able to produce enough supply of critical minerals for US automakers with enough time and capacity to meet a competitive threat that is not just an urgent priority but has arguably a decade head-start.

The US government released proposed guidance to provide clarity and certainty around the IRA’s foreign entity of concern (FEOC) requirements — which apply to both mining and processing of minerals — in December 2023, including:

a 25% or more ownership threshold of the entity’s board seats, voting rights, or equity interest that are cumulatively held by an other entity, whether directly or indirectly via one or more intermediate entities

manufacturers to conduct due diligence that complies with industry standards of tracing for battery materials

The restrictions for battery components begin in 2024, and for critical minerals extracted, processed or recycled by a FEOC, start in 2025.

These restrictions would mean that even some companies operating in free-trade agreement (FTA) countries, such as Australia, are unlikely to qualify for the tax credits. For example, the Greenbushes mine, the world's largest producer of lithium concentrates, is 26% owned by Chinese-owned Tianqi Lithium.

Only a fifth of the 103 EV models currently on the market qualify for the whole tax credit in the US under the latest rules.

US automakers have already pushed back against the restrictions on critical minerals, for example:

Ford announced a direct stake in an Indonesia battery-nickel plant, with Indonesia’s PT Vale and China’s Huayou Cobalt — just days after the proposed FEOC guidance released in December 2023 and despite threats of investigation by Congress

the US Alliance for Automotive Innovation is lobbying against an “overly broad” application of FEOC, urging for vehicles with insignificant traces of Chinese material to be eligible for the tax credit

Tesla warned they may have to raise prices on their EVs

The US Treasury and Department of Energy have already provided “temporary” exemptions for some trace critical minerals from FEOCs until 2027. The reason was described probably most aptly by a statement by the Alliance for Automotive Innovation:

“The EV transition requires nothing short of a complete transformation of the US industrial base. It’s a monumental task that won’t happen overnight.”

However, Republican lawmakers argue against such exemptions, for example Senator Joe Manchin promised to "take every avenue and opportunity to reverse this unlawful, shameful proposed rule."

“At a time when China is using massive subsidies to undercut U.S. manufacturers and throttle the global market for battery components, Treasury’s naïve new regulations would open the floodgates for American tax dollars to flow to Chinese companies complicit in trade violations and forced labor abuses”

— Representative Mike Gallagher of Wisconsin, chairman of the House Select Committee on the Chinese Communist Party, said

And, as we have warned in our recent analysis, “America's current critical mineral strategy threatens disaster”, it will be very difficult to stop cheap, almost untraceable critical minerals finding their way into a market where they are overvalued.

Conclusion

US automakers, US miners and the US government all want the same thing: investment in a secure supply of critical minerals.

US automakers, facing an urgent existential threat, need the minerals now, and at competitive prices.

If the US government backs down on enforcing its FEOC guidelines to accommodate the US automakers urgent need for access to critical minerals, wherever they are sourced, then, as one mining CEO told us: “It’s over.”

The problem is that US miners and their FTA partners are also facing an urgent, existential threat of their own, from cheap Chinese supply. To secure supply, mines need the government to support legislation that drives financial investment in the face of such competition. But, because of the time it takes to develop new mines, every year such incentives are delayed, the harder it is to make a transition away from cheap supply from elsewhere.

And, without a secure source of critical minerals, American automakers and the government will also be at the mercy of Chinese supply.

If the FEOC restrictions (and net-zero targets) are, to some degree, maintained, (we are sure there will some give-and-take over exact FEOC ownership percentages), then pressure to dramatically expand investment in critical mineral mining across the US and its FTA partners will increase significantly.

A second trade war is coming. If American automakers and miners fall out, then the critical mineral trade war — and with it the EV trade war — with China is lost. If they align forces, there is an opportunity to stay competitive. To paraphrase the old adage: divide and fall, unite and thrive.

🚀 Please smash the ♡ button, subscribe for the banter ✓ and share with friends and colleagues. We are always grateful for your comments and support.

It appears very likely that their will be significant road 🚧 in Congress's and tge Administration's way to fulfill their goals. Very much a self sabotage if the rules are followed 100%, as you elaborate. The interesting thing is it will be Congress that actually will solve these issues. We are already seeing the walk back or modification in several regulations for light duty & medium to heavy duty vehicles, we see a push for faster connections to the grid, etc. See what happen recently with Cleveland Cliffs purchase of Untied Steel & transformer regulations. The issue than becomes that of time, will all the maneuvering be enough for the time frame they want. The answer is an unequivocally NO, so then why go thru this, when all they have to do it roll out the red carpet for CANDU reactors, unleash oil & gas drilling, and work on greater efficiency regulations.

I don’t own and do not aspire to own an EV. Whilst I’m a small survey, I do wonder whether peak EV is getting closer than most people think ? Those who want an Ev have probably already got one ?