Lessons on hydrogen energy's ambition vs reality from South Korea

6.2m FCEVs targeted by 2040, but only 29,733 on the road in South Korea by 2022

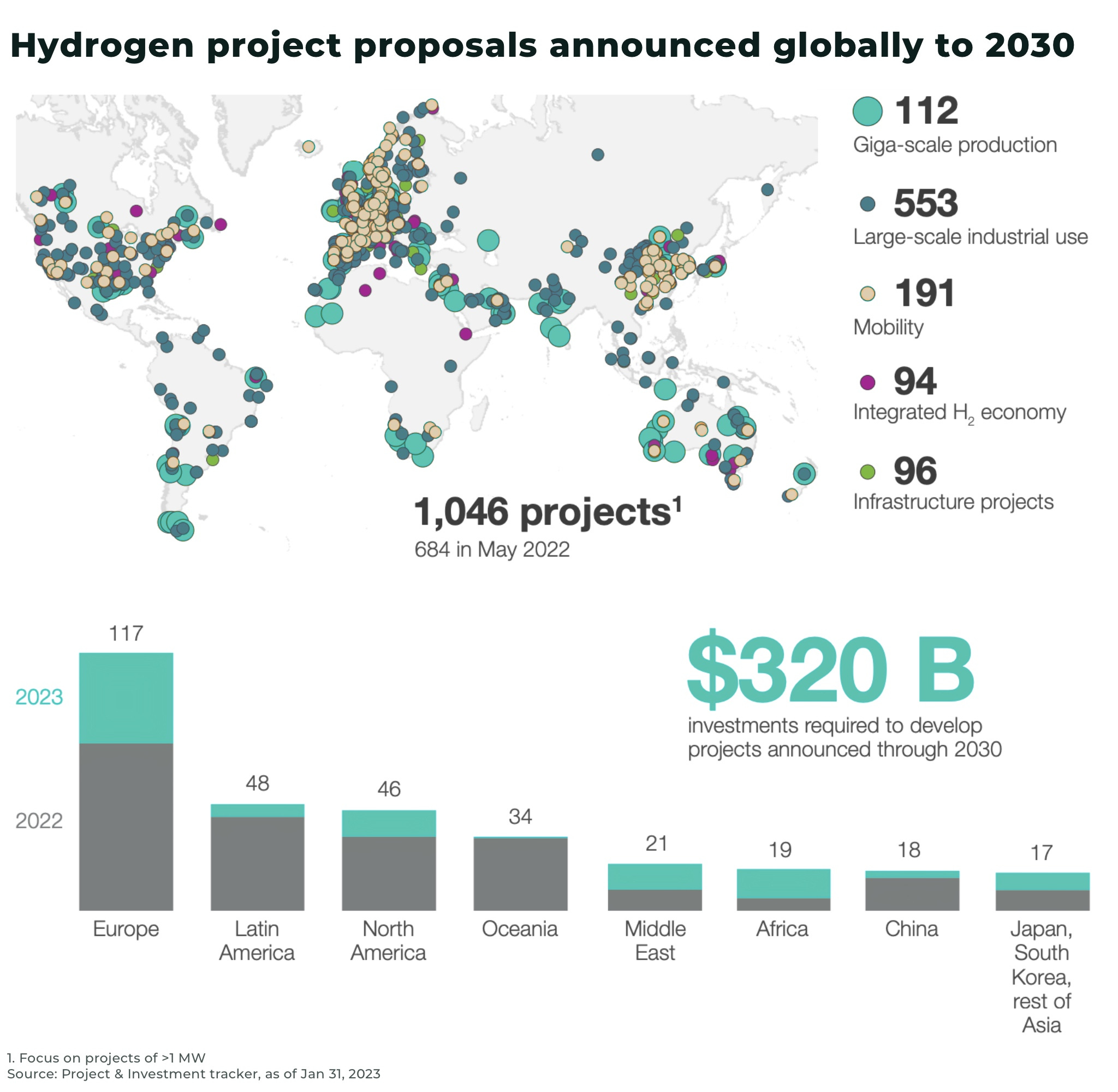

$320 billion of global hydrogen investments announced up to 2030

South Korea hydrogen roadmap targeted 6.2million fuel cell electric vehicles by 2040 but South Korea had only 29,733 FCEVs by 2022

use in heavy industry and ammonia seeing traction in South Korea's hydrogen market

🚀 Please smash the ♡ button, subscribe for the banter ✓ and share with friends and colleagues. We are always grateful for your comments and support.

The US is investing US$7billion to leverage nearly US$50 billion in private investment for the launch of seven hydrogen hubs across the country.

"The nearly US$50 billion investment is one of the largest investments in clean manufacturing and jobs in history"

— The White House, Regional Clean Hydrogen Hubs to Drive Clean Manufacturing and Jobs

And the US is not alone: 1,000 hydrogen project proposals have been announced across the world, representing US$320 billion of direct investments to 2030 — up from US$240 billion last year. By 2050, it’s estimated global hydrogen trade between major regions can generate more than US$280 billion in annual export revenues.

But there's a problem. Hydrogen is difficult. Very difficult. We've seen multiple false dawns for the technology before. So, can it work this time?

One frontrunner in betting that hydrogen energy is the future is South Korea.

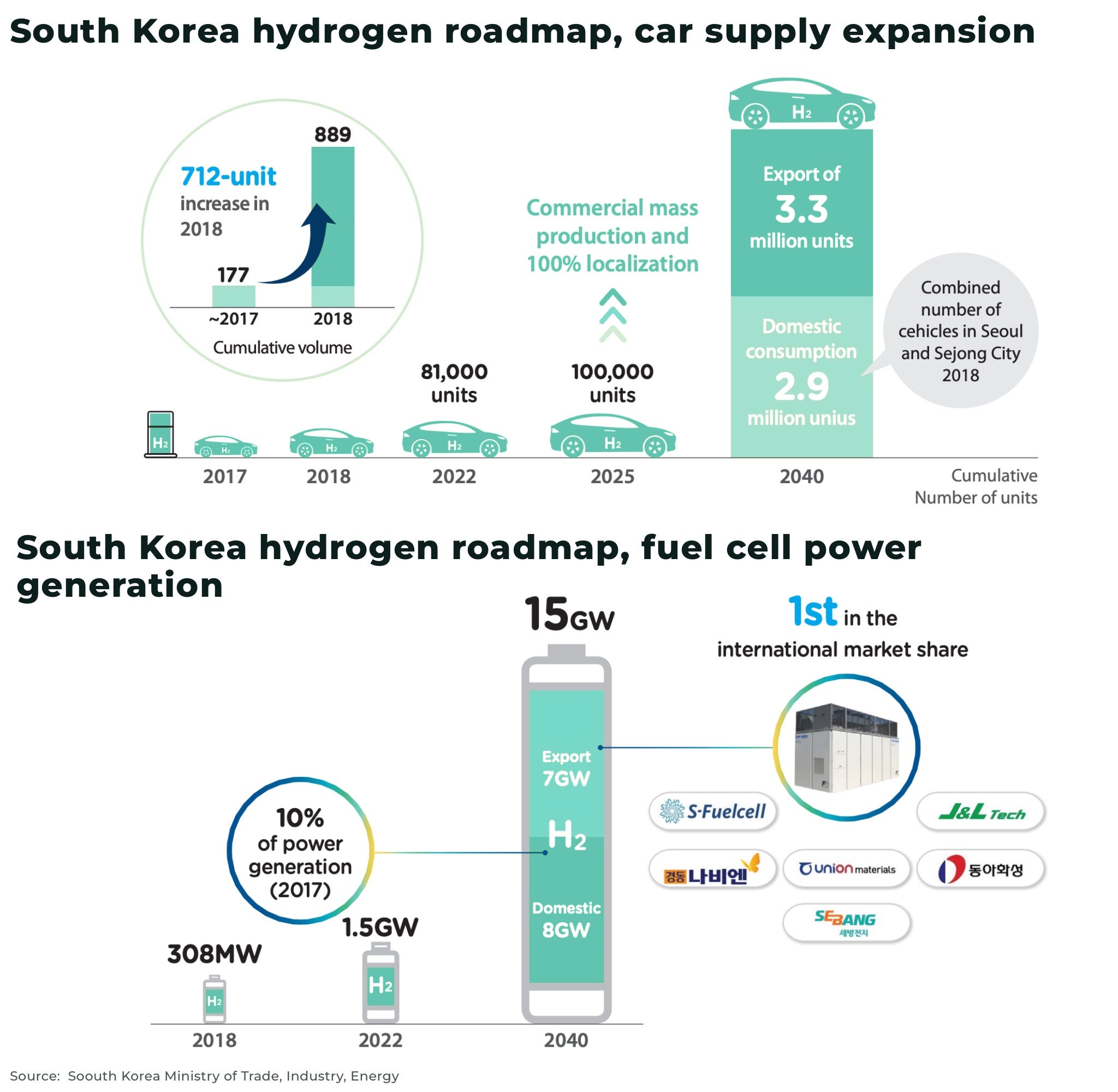

In 2019, South Korea announced one of the world's most ambitious national hydrogen strategies, the Hydrogen Economy Roadmap, with production targets of 15GW of fuel cell power generation, 6.2million fuel cell electric vehicles (FCEV), 1200 refilling stations, 41,000 hydrogen buses, by 2040.

So, what does the country's efforts since 2019 tell us about the feasibility of hydrogen energy for the US and rest of the world.

Hydrogen energy

Firstly, why hydrogen energy?

Hydrogen is the most simple, abundant and lightest element in the universe. When it combusts, it has the highest energy content of any common fuel by weight (x3 higher than gasoline), without releasing carbon dioxide when burned.

Hydrogen is essentially a store of energy, produced by another energy source, which can then be used as a fuel to power vehicles, from cars to planes, to reacting to make the extremely high temperatures needed to make steel, as well as being used in refining and chemical sectors, such as to make ammonia and fertilizer.

Hydrogen comes in a variety of “color” types, including:

Green hydrogen, made via electrolysis which splits water into hydrogen and oxygen using renewable energy, such as solar or wind, so the entire production cycle is carbon neutral

Grey hydrogen, made using natural gas or methane which releases carbon dioxide into the atmosphere

Blue hydrogen, also made from fossil fuels, but any carbon emissions released are captured and stored

(Read our Introduction to investing in hydrogen energy for more details)

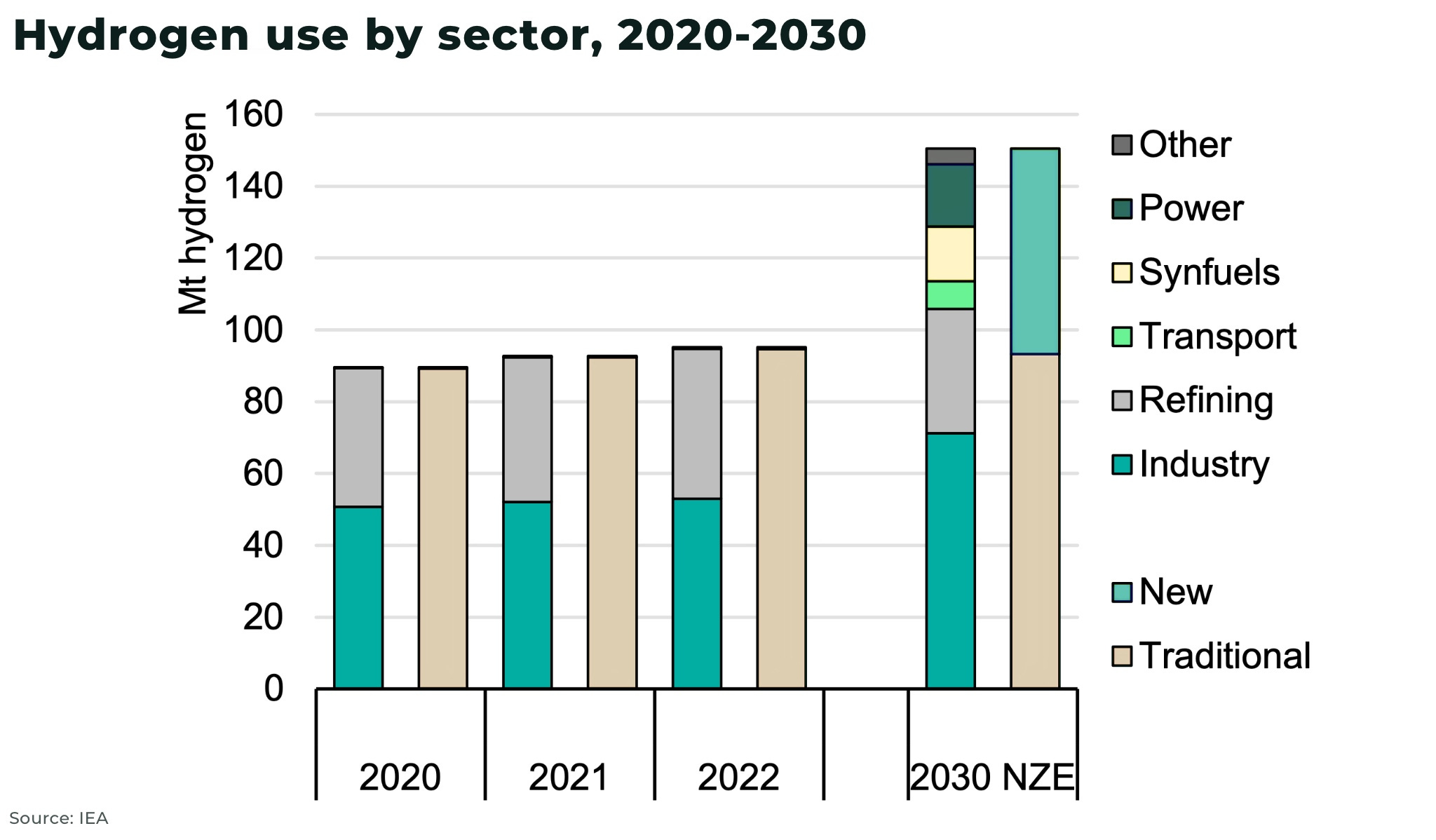

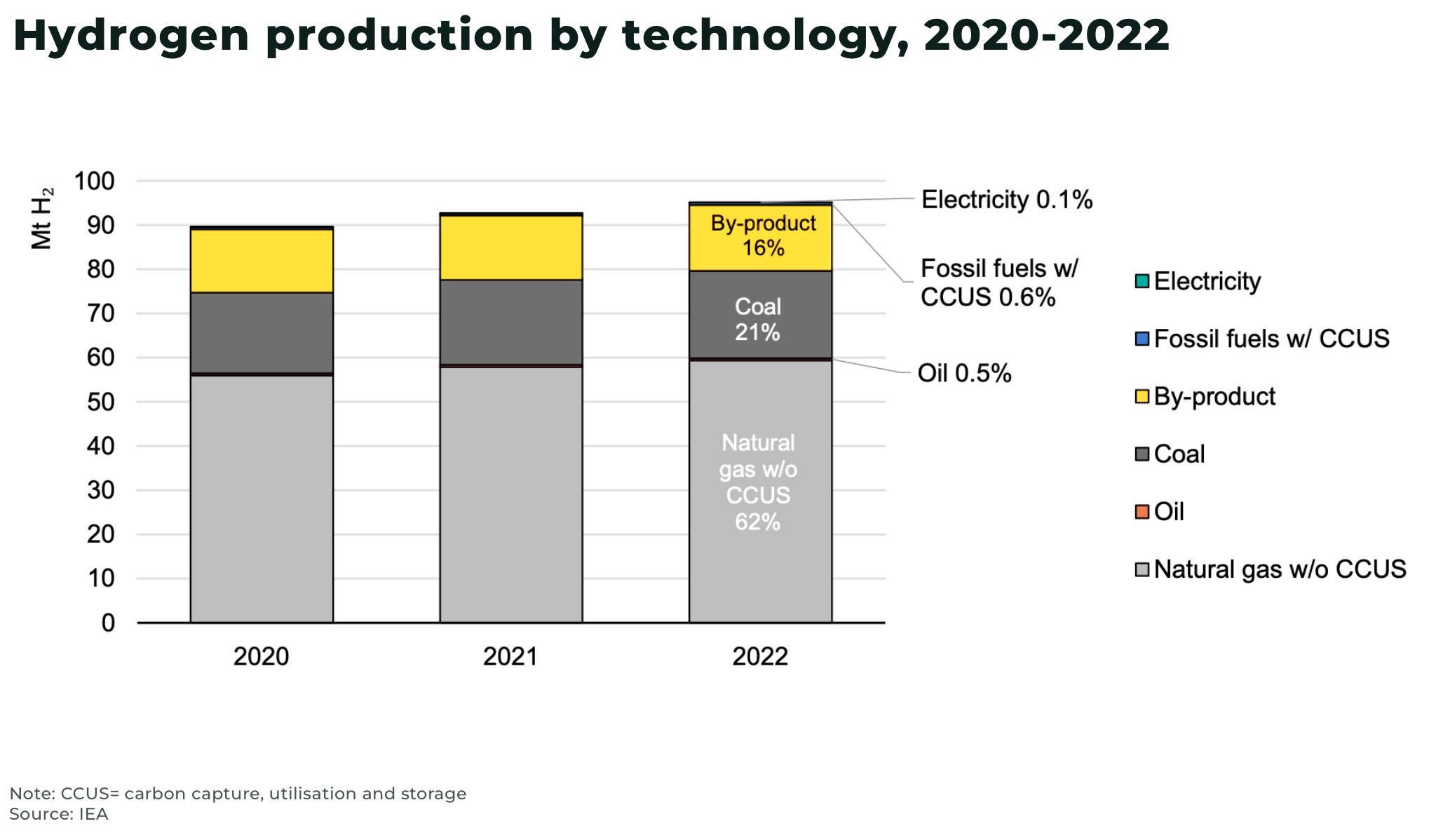

One of most significant challenges for hydrogen to replace fossil fuels, is that low-emission hydrogen production in 2022 was less than 1 Mt, or 0.7% of global production. The majority is made with natural gas.

South Korea’s hydrogen roadmap

The government in South Korea has not been lacking in ambition with its hydrogen roadmap, working to become a global leader in the industry, with estimates that:

its hydrogen energy investment will create 420,000 jobs and support US$43billion to the national economy by 2040, equivalent to 2.5% of the country’s GDP in 2017

the amount of energy consumption replaced by hydrogen is expected to equal 5% of total expected energy consumption by domestic households in 2016

To do this, South Korea hopes to leverage its industrial base with regulation and financial incentives to rollout the new hydrogen tech and infrastructure. This includes:

priority focus on market creation, increasing demand for hydrogen from 130,000 tons/year in 2019, to 470,000 tons/year in 2022, to 5.26 million tons in 2040, potentially one of the world’s largest market share in hydrogen fuel cells and FCEVs

establish domestic production with targets for 60% self-sufficiency by 2050, and overseas contracts to ensure supply is 100% clean hydrogen by 2050. For example,

South Korea plans to invest US$4.5 billion in a green hydrogen project Canada

South Korea and Australia are partnering to build a sustainable hydrogen hub in Wetern Australia, including US$25 billion investment by steelmaker Posco in green hyrogen and green steel, and at least US$6.6 billion investment by an Australian-South Korean consortium

invest US$192.7 million to build x6 “hydrogen cities”, including a new blue hydrogen project and port

introduce a hydrogen power generation bidding market, with the first auction for a total of 1,300GWh of electricity produced from “general hydrogen”

introduce a new hydrogen certification system in 2024 to incentivse clean hydrogen

international partnerships, for example with Japan, including collaboration to leverage their ability to negotiate price for hydrogen fuel

the Environment ministry has reportedly requested US$262 million to help finance the purchase of 1,500 hydrogen buses in 2024

There are an estimated US$17 billion of investments in hydrogen across South Korea and Japan, and another US$34billion throughout the Oceania region.

No one's buying

The challenge is that South Korea is struggling to meet it’s own targets.

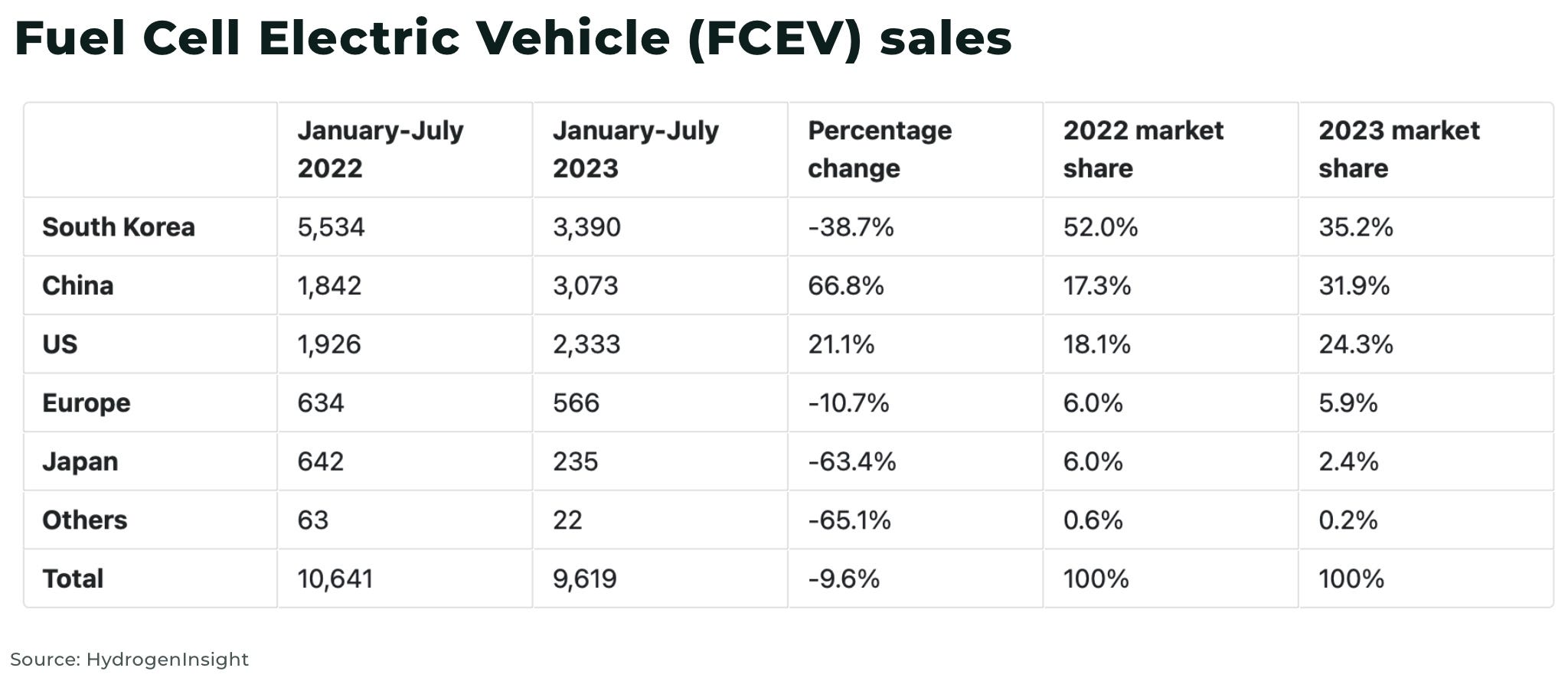

The country is the global leader in market share of FCEVs — with 29,733 FCEVs on the road in 2022 — but the number of vehicles sold dropped from 5,534 in H1 2022 to 3,390 in H1 2023. With the exception of China, worldwide sales fell 9.6% year-on-year. A far cry from the 6.2 million targeted by South Korea's roadmap for 2040.

In comparison, sales of electric vehicles in South Korea are projected to reach 1.8 million units in 2023, an increase of 3.3% in 2022.

“At this point the government has realised that developing good fuel cell cars, that’s not enough,” he said. “We have to construct all the infrastructure as well, including charging stations. And if you have all the charging stations, where can you get the hydrogen gas? Right now, it is made from natural gas, fossil fuels, but to really make a contribution to the carbon-free society we have to get this hydrogen from a carbon-free energy source, renewable energy. But it is very expensive”

— Nam-hoon Kang, chairman of the Korea Automobile Mobility Industry Association (KAMA)

Last year, South Korea announced significantly revised targets for it’s Hydrogen Economy Roadmap, including:

30,000 hydrogen-powered commercial vehicles by 2030

70 liquid hydrogen fuel stations by 2030

clean hydrogen being 7.1% of the country's energy mix by 2036

Despite a target of 1.5GW clean hydrogen power generation by 2022, hydrogen is not listed as any of the ten energy sources providing South Korea’s power in 2021.

These challenges with hydrogen energy are not unusual to South Korea, for example:

planned hydrogen projects in Germany are on track to have 8.7GW capacity by 2030, only a small increase from an 8.1GW estimate in February, significantly slower than the increase in 2022

a consortium of oil majors and utilities have “shelved” plans to build a 700MW blue hydrogen project in the UK

a German state-owned train company that launched 14 hydrogen trains in 2022 has already abandoned the project

US green hydrogen tech firm Plug Power warned it may fold in the next year due to continued operating losses

in France, the first town to use x8, 18-meter fuel-cell buses, is planning to switch to electric

and, so far in 2023, hydrogen-related funding tracked by Hydrogen Insight is far behind the pace of hydrogen investments in 2022

The challenge of costs

The biggest hurdle to widespread, faster adoption of hydrogen is cost.

Inflation and interest rates, as well as supply chain problems, have increased costs of capital, financing, labor and equipment — and so, hydrogen is struggling to gain traction against cheaper alternatives.

Only 5% of new low-emission hydrogen projects have received firm investment decisions.

The problem: hydrogen projects are very upfront capital intensive (as the lightest molecule, it is extremely difficult to transport, as well as being very flammable), making them especially sensitive to any rise in costs. For example, an increase of 3% in the cost of capital could raise a hydrogen project costs by nearly one-third. With governments constrained by rising yields, announced government funding will likely be able to support a smaller number of projects than previously expected.

An estimated 76% of global hydrogen is made with natural gas — “grey” hydrogen — and, although costs of natural gas have fallen from the highs after Russia’s invasion of Ukraine, they still remain elevated, with costs passed on to hydrogen consumers. In California, hydrogen prices have increased to US$36/kg in 2023, from US$13.14/kg in 2021.

For green hydrogen, costs have increased as wind and solar energy struggle against rising interest rates. And for electrolyzers, an estimate by the Financial Times, suggests: "today, inflation has pushed up the price to about $1,500 per kW but it could be as low as $250 per kW by 2050. Using a midpoint of $875 per kW implies a capex requirement of $7tn to achieve the desired goal.”

To meet net-zero targets, it’s estimated US$9 trillion will need to be invested in the global hydrogen supply chain, but this is likely to rise with interest rates and delays in government clarifying both funding and national regulations for hydrogen.

Lessons from South Korea for hydrogen investors

Investment risks are a part of any nascent industry, and South Korea’s first mover advantage offers both a warning and opportunity for investors.

Firstly, as we highlighted at the top of this analysis, hydrogen is difficult, very difficult. And it will likely cost much more and take longer than expected.

Any investor looking for exposure to hydrogen must look to the long-term.

But, as South Korea’s doubling down on it’s economy roadmap highlights: for an industrialised economy looking to decarbonize (especially as Cross Border Carbon Tariffs are introduced), hydrogen will be a critical part of the energy mix — but in specific sectors of the economy, rather than across the entire economy as some of the hype might suggest.

Despite the country’s renewed push to improve private ownership of FCEVs, we do not think the market will have much success against electric vehicle competitors — and this is especially so in the rest of the world where government investment in FCEV infrastructure is significantly less prioritzied than in South Korea. There is an argument for hydrogen powered public transport, from buses to trains, but South Korea’s rollout offers another warning abotu the difficulties.

Two areas we would highlight are showing signs of significant potential for hydrogen in South Korea (and elsewhere), are heavy industry and ammonia.

Hydrogen and heavy industry

there are very limited options to reach the required temperatures to produce zero-emission steel. And so, South Korea’s leading steelmaker, Posco, aims to complete a 300,000 tonnes/year hydrogen reduction steelmaking plant by 2026 and introduce a 1 million tonnes/year commercial production plant by 2030

Korea Zinc’s giant Ulsan refinery is powered by an onsite generator that burns methane gas. The company promises to fully power its refinery with “renewables”, including green hydrogen, by 2040, and its Korean refinery by 2050

Korea Electric Power Corp, steelmaker POSCO Holdings and Lotte Chemical have signed a letter of intent with Saudi Aramco for a US$15bn blue ammonia production project

a consortium including South Korea's top steelmaker POSCO and France's Engie are planning a US$7 billion project in Oman to export 1.2 million tons of the green fuel to South Korea by the mid 2030s

As this infrastructure is built out, grey hydrogen will continue to be the predominant type of hydrogen used in the country.

Hydrogen and ammonia

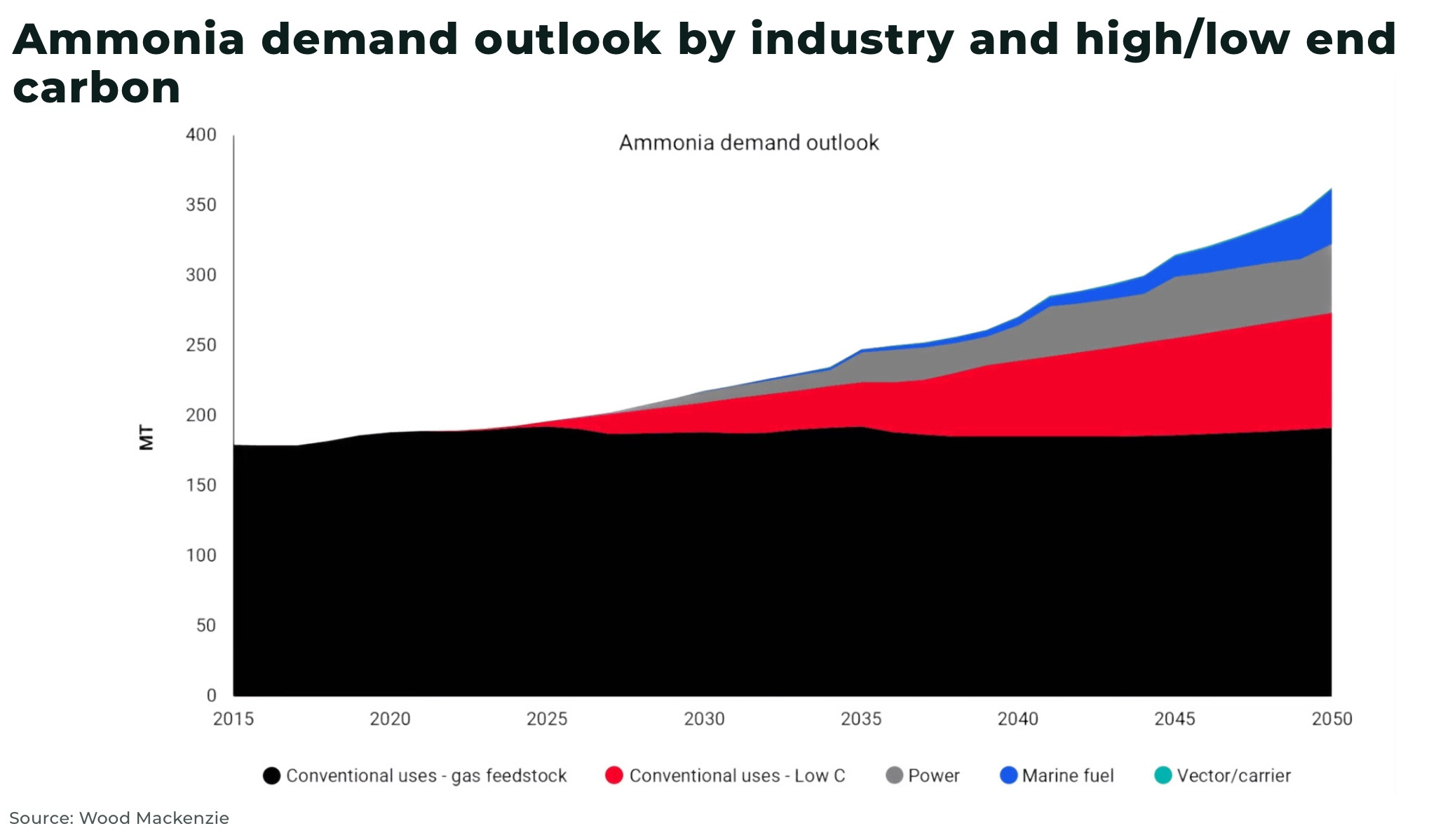

Ammonia a low-cost and simple option to store (through the Haber-Bosch process), transport and trade hydrogen, especially over long distances, with the potential to “crack” and reconvert it back to hydrogen at it’s destination. And it is already widely used in the fertilizer and chemical industry.

180 million metric tons of ammonia are produced every year. This means a global infrastructure, including 120 ports with ammonia terminals, is already set up.

Deloitte estimates the breakeven point for clean hydrogen can be reached before 2035 for pure hydrogen and ammonia, with ammonia demand reaching more than 590 MT by 2050.

South Korea is already expanding it’s global ammonia supply chain:

build an ammonia receiving terminal, that can handle 4 million tons a year, in areas where there is a high concentration of coal-powered plants, including Incheon, Gangwon and South Gyeongsang, by 2030

South Korea and Japan are set to announce a joint supply network for hydrogen and ammonia

South Korea’s SK ecoplant Co plan to develop US$15 billion green hydrogen project in Canada, one of the largest such projects in the world, has been approved

last year, the world’s first commercial shipment of “clean ammonia” was transported 14,000km over 20 days from Saudi Arabia to South Korea, with plans for another this year

Korea Electric Power Corp, steelmaker POSCO Holdings and Lotte Chemical have signed a letter of intent with Saudi Aramco for a US$15bn blue ammonia production project

a consortium including South Korea's top steelmaker POSCO and France's Engie are planning a US$7 billion project in Oman to export 1.2 million tons of the green fuel to South Korea by the mid 2030s

Australia-based Origin and Posco have signed an MOU to cooperate on producing and supplying green hydrogen in the form of green ammonia

South Korea plans to commercialize ammonia-fueled power generation by 2030

Hyundai’s HD Korea Shipbuilding & Offshore Engineering reported two orders for a total of four very large ammonia-fueled carriers (VLACS) valued at a total of US$463 million to be built at the shipyard in Ulsan, South Korea

It’s estimated nearly half of the contracted hydrogen volume is planned to be delivered in the form of ammonia by 2030. South Korea and Europe are the largest export destinations.

In 2022, green ammonia made up the largest proportion of global hydrogen project announcements at 27%.

Conclusion

With more than US$320 billion of announced investments into hydrogen energy, there are a significant number of opportunities for investors.

However, as we have highlighted with our analysis on renewable energy vs interest rates, the market is shifting and risks for investors have increased.

As always, a technological breakthrough or sharp economic downturn would have a significant impact on the market and any projections.

The experience of South Korea as it tries to navigate it’s ambition for hydrogen energy and the practical challenges rolling it out, offer investors important insights into the market.

For investors looking for exposure to the hydrogen market, heavy industry and ammonia sectors offers significant upside in a mature market, with infrastructure that can be, over the medium-term, repurposed.

Stay subscribed.

🚀 Please smash the ♡ button, subscribe for the banter ✓ and share with friends and colleagues. We are always grateful for your comments and support.

Good article, thank you.

I am retired chemist. I can assure that a kg of H2 contains a significant amount of potential energy.

The problem is that it takes more energy to produce a kg of the stuff than it intrinsically contains. Then there is the issue of storing and transporting, amoung other problems that also require even more energy input, likely from fossil fuels.

The Laws of Physics and Thermodynamics still hold, but that is ignored typically these days for the "Green Agenda".

Hydrogen still has value as a locally produced feedstock for other processes.

If it was produced from nuclear driven electrolysis, that would be an advantage.

> without releasing any greenhouse gases, including carbon.

Water vapour is considered a greenhouse gas, correct?