Graphite mining at turning point

Investment Insights. Commodities. Energy Transition.

demand for graphite from EVs and batteries will rise almost x10 by 2032

batteries require larger volumes of graphite than nickel, cobalt or lithium

decarbonisation drive needs new supply of graphite outside China

Natural graphite is a critical element for electric vehicle batteries and energy storage systems and it’s facing a potential 1.2-million-metric-ton supply shortage in 2030, rising to 8 million tons by 2040.

This is one of the largest shortfalls of any battery metal, but until now graphite has attracted much less attention than nickel, lithium or cobalt.

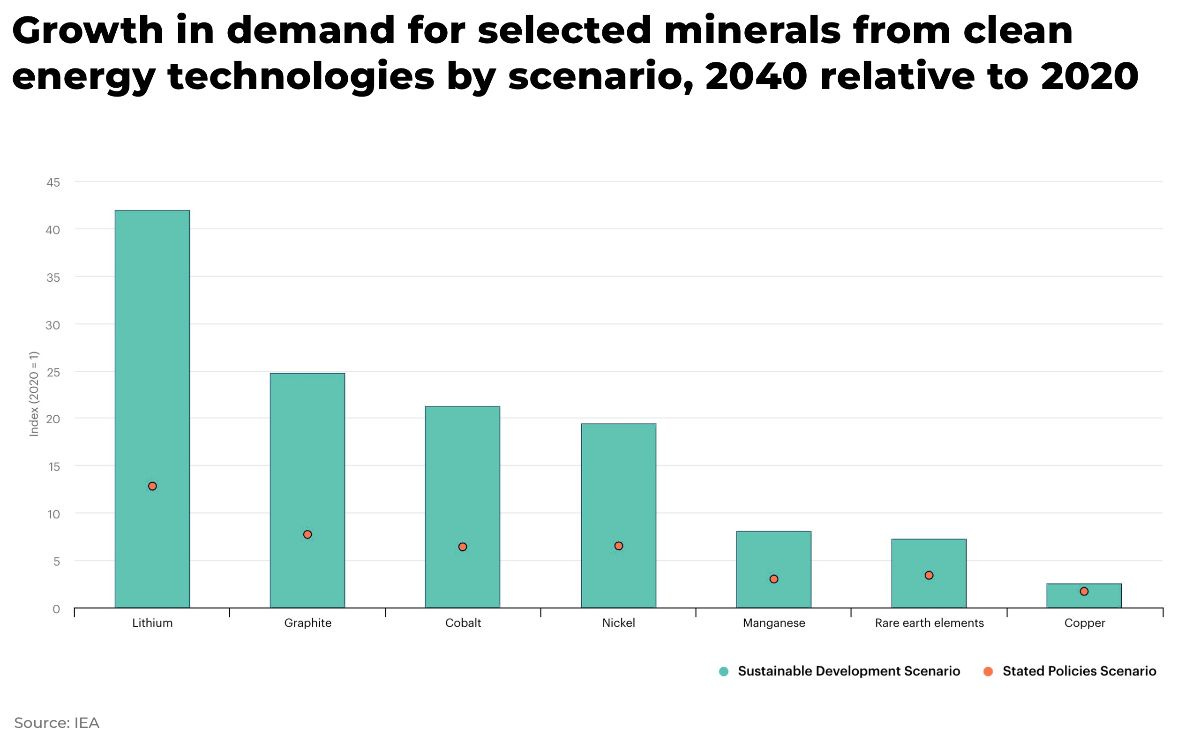

Between 2020 and 2040, demand for graphite is expected to climb 25-fold, outstripping the rate of growth for both cobalt and nickel, as countries, companies and consumers race to decarbonize.

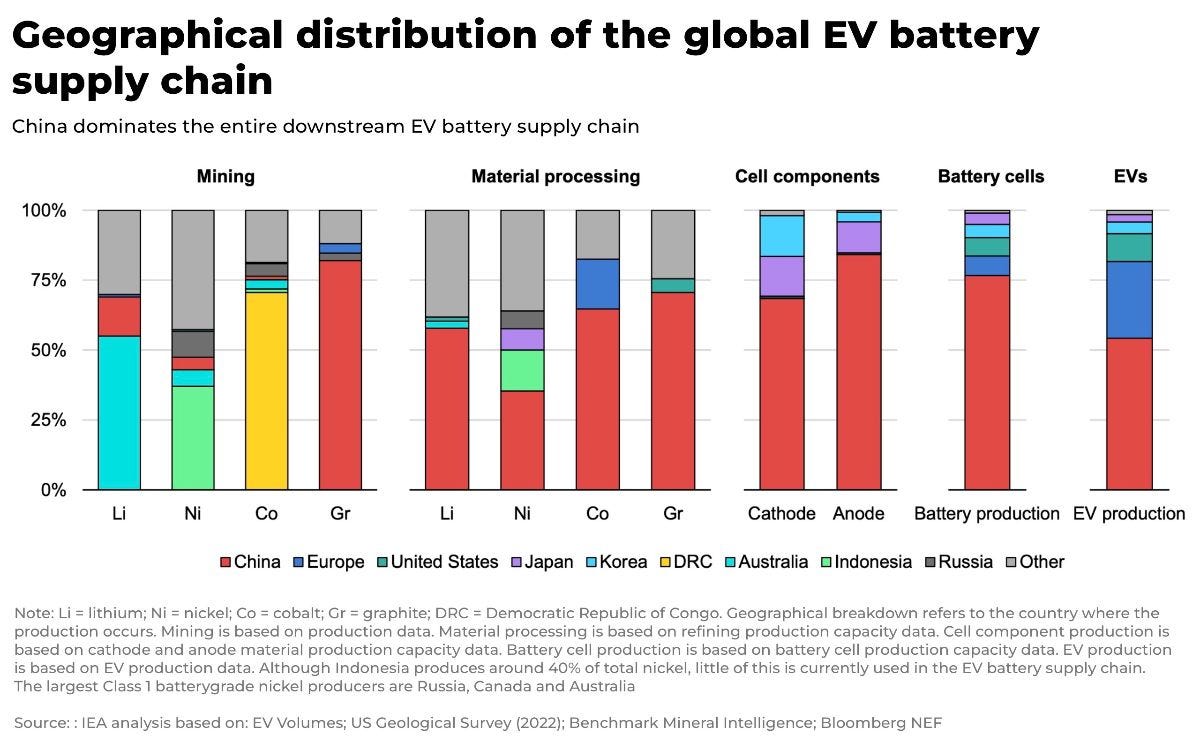

China currently dominates the market for graphite, much like almost every other battery metal, but this dominance provides a strategic opportunity for western producers and investors.

What is Graphite?

There are two main types of graphite that are used in applications, from pencils and lubricants, to the electrodes that are part of electric arc furnaces in the steel industry.

natural graphite (which is mined)

synthetic graphite (produced from petroleum coke under high temperatures)

Natural graphite is especially in demand: it’s cheaper to produce (it only needs to be mined, not synthetically produced), as well as more environmentally friendly (it is usually purified using hydrofluoric acid and sodium hydroxide but does not require large amounts of petroleum coke and the subsequent carbon emissions) to produce.

China and Graphite

Currently global supply is dominated by China.

China produced 820,000 metric tonnes of natural graphite in 2021, according to the US Geological Survey, against world production of only 1 million metric tonnes — 82% of global production.

However, China’s dominance of global output is increasingly at odds with US and European aspirations to secure both the supply chains for critical commodities and the economic opportunities of the energy transition.

So far, graphite has attracted less economic and geopolitical interest than other critical materials because prices have not yet responded to the huge growth in demand from the battery sector.

As demand rises and supply tightens, so sentiment — both politically and financially — is moving.

According to Andy Miller, COO of Benchmark Mineral Intelligence, “both the mined and synthetic graphite market is at a turning point.”

We agree.

Investment in graphite production will be increasingly driven by the West’s response to secure their supply chains in the energy transition, not just to compete against China’s dominant position in global graphite production, but also in response to Covid lockdowns and Russia’s invasion of Ukraine.

For example, graphite has been named a “critical mineral” in the 2021 Defense Production Act and the 2022 Inflation Reduction Act in an effort to boost domestic production. This means graphite mining companies can now seek production credit equal to 10% of production costs.

The act also specifies that at least 40% of critical minerals in US-made electric vehicle batteries must come from US miners or recycling plants, or mines in countries with free trade deals with the US. This requirement will rise by 10% each year, to a maximum of 80% by 2027.

For example, the Department of Energy has issued a US$102 million loan to Syrah Resources in Louisiana to produce the first domestic battery-grade natural graphite active anode. It’s a material the US is currently 100% reliant on China.

And, as we have flagged with other critical metals, there is an increasing demand — and opportunity for Western companies — for “environmentally-friendly” graphite. In particular natural type graphite.

Producing 1 kilogram of natural graphite in China emits approximately 16.8 kg of CO2e.

In Canada, miner Northern Graphite Corp has produced anode-grade graphite with a carbon footprint of 9.5 kilograms of CO2e, far less emissions than anode-grade synthetic graphite production in China.

There will be volatility, especially in the short-term. But electric vehicles and the energy transition have created new opportunities for investors in the medium and long-term.

By 2032, demand for graphite from the battery sector will rise to 3 million metric tonnes, market intel provider Fastmarkets forecasts, up from 350,000 metric tonnes in 2021. At current prices of just under $3,000 per metric tonne, that equates to a market worth $8.4 billion.

But these prices may well rise as with an impending supply gap. Graphite producers listed on western exchanges are sounding the alarm.

“The dynamics and speed at which supply and demand are getting into imbalance are unprecedented” — Shaun Verner, CEO, Syrah Resources

"Globally, we produce 1.3-1.4 million mt/year [of graphite], but most of that goes to applications other than energy storage (10-15%)... By 2030, it is estimated that another 4-5 million mt/year of graphite will be needed. Conservatively, around 3.5 million mt/year"

— Tirupati CEO Shishir Poddar told S&P Global Platts

And the G20’s Financial Stability Board has warned of weaknesses in commodity markets with a “significant” concentration of firms, banks, exchanges and clearing houses threatening to transmit losses to the wider economy.

It’s not just electric batteries

Demand for graphite is not only fueled by electric batteries. Smartphones, solar panels, ceramics, polymers and much more.

But, more importantly, it is essential for graphene, a one-atom thick layer of carbon atoms layered in a hexagonal lattice, considered one of the strongest materials in the world. It’s 200 times stronger than steel, but more flexible and lighter. It is the building block of graphite and can be molded into any shape.

It’s a material still in its early stages of industrial and commercial development, but one with significant potential. One estimate, puts the global graphene market as USD 556 million by the end of this year and is projected to register a CAGR of over 38%

Exposure to graphite

It’s difficult to get a consistent figure on the price of graphite. The reason is that it’s not traded on an exchange, so investors can’t get exposure to the physical material.

Instead, miners often set up “offtake agreements” where buyers agree to take agreed amounts of graphite over a specific period of time.

This can feel like investing in the dark if you don’t know how much a mine can sell it’s graphite production.

But, for investors looking to invest in graphite upstream, the best way is investing in exploration and mining companies. Downstream, we recommend looking to electric car and battery companies.

For investors that want a starting place, here are suggestions of three Western companies that are producing or near-producing, with market capitalizations equivalent to at least $200 million and have commercial deals in place already for material that will be refined to the specifications that battery-makers require. They all have carbon mitigation and management schemes, which is critical if the use of batteries is to play its intended role in decarbonization.

Syrah Resources (ASX: SYR) aims to be a vertically integrated supplier of graphite from its Balama operations in Mozambique, which produced 163,000 metric tonnes of graphite last year, and its planned processing facility in Vidalia, Louisiana. It is negotiating a $220-million grant from the Biden administration for Vidalia and has agreed the specification of graphite anode materials to supply Tesla from the planned plant.

Nouveau Monde Graphite (NYSE: NMG) plans to be North America’s largest integrated producer of graphite for lithium-ion battery anodes. Between this year and 2025 it aims to launch production of around 100,000 metric tonnes per year of graphite from its Matwinie mine near Montréal and around 46,000 metric tonnes per year of graphite anode material. It has signed a non-binding deal with battery producer Panasonic to supply it with battery materials.

Talga Group (ASX: TLG) owns the Vittangi graphite project in Sweden where it expects construction to start this year after the successful completion of a 25,000 metric tonne trial mine. It is building a natural graphite anode plant that will run on renewables from which it expects to produce 19,500 metric tonnes per year of coated graphite anode from 2024. It has signed a non-binding deal to supply Verkor, which is being backed by the Renault Group and others to build a lithium-ion gigafactory in France.

DISCLAIMER:

The Oregon Group has full editorial control over all content published on this website and the author has not been compensated or remunerated by any person to provide content for The Oregon Group, and all statements and expressions herein are the sole opinion of The Oregon Group. However, from time to time, The Oregon Group and its directors, officers, partners, employees, authors, or members of their families, as well as persons who are interviewed for articles on this website, may have a long or short position in securities or commodities mentioned and may make purchases and/or sales of those securities or commodities in the open market or otherwise. By accessing and using this website, readers are cautioned to assume that each of the foregoing persons may have a financial interest in all companies and sectors mentioned on this website. Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable., and any such statements are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities or commodities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and The Oregon Group undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material. The information provided on this website is for informational purposes only and is not, directly or indirectly, an offer, solicitation of an offer and/or a recommendation to buy or sell any security or commodity, and the information provided on this website should not be construed as any advice or an opinion as to the price at which the securities of any company or commodity may trade at any time. The Oregon Group is a publisher of financial information, not an investment advisor. We do not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient, and the information provided on this website is not and should not be construed as personal, financial, investment or professional advice. Readers are cautioned to always do their own research and review of publicly available information and to consult their professional and registered advisors before purchasing or selling any securities or commodities and should not rely on the information contained herein. Neither The Oregon Group nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein. By using the Site or any affiliated social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.